How Conflict-of-Interest Regulatory Frameworks Are Catching Up to the Curator Model

Series: DeFi Infrastructure for Institutions

P2P.org's content series for regulated institutions evaluating on-chain capital allocation. Each article addresses a specific infrastructure, governance, or compliance dimension that determines whether a DeFi allocation can clear institutional approval and operate within mandate.

This is the third and closing article of the regulatory trilogy examining the external pressure making institutional-grade vault governance a requirement rather than an option. The first article examined what MiCA means for DeFi vault operators and institutional allocators. The second article examined Travel Rule enforcement and the on-chain compliance gap. This article examines how conflict-of-interest frameworks across MiFID II, AIFMD II, and IOSCO's DeFi-specific recommendations are converging on the same structural problem: the DeFi vault curator model creates conflicts of interest that existing and emerging regulatory frameworks now require to be identified, documented, and managed.

The second article of this series established that the DeFi vault curator model creates a structural conflict of interest: curators are incentivised by TVL growth and performance fees, not by mandate alignment with any individual depositor. The architecture places no independent check between their decisions and on-chain settlement. That conflict was examined as a governance problem in the first trilogy of this series.

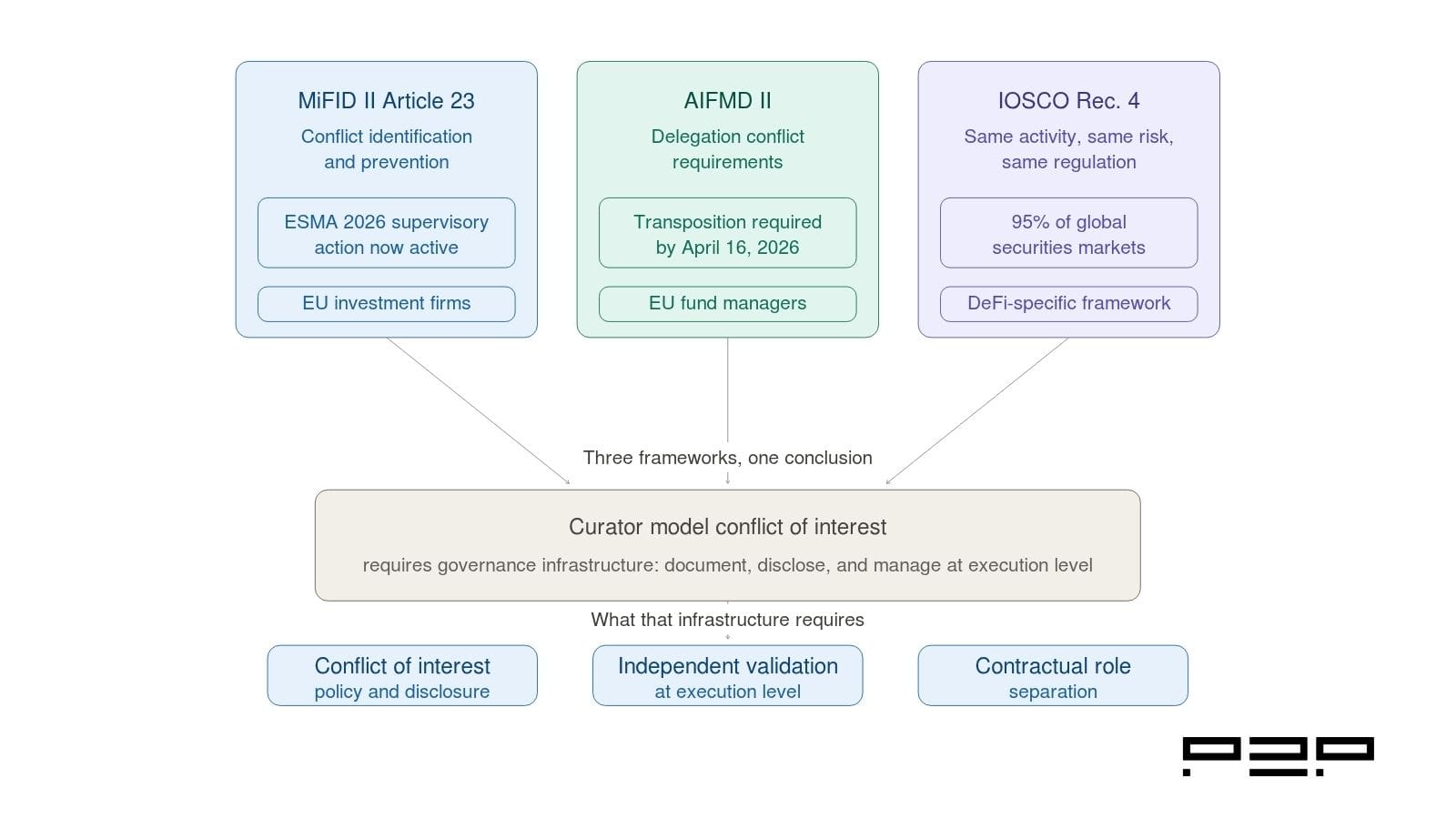

What this article examines is a different dimension of the same problem: the conflict of interest in DeFi vault design is not just a governance gap. It is increasingly a regulatory gap. Three distinct regulatory frameworks, developed independently, in different jurisdictions, for different purposes, are converging on the same conclusion: the arrangement where a single entity designs an investment strategy, executes it, and benefits from its performance without independent oversight creates conflicts of interest that regulated institutions cannot accept and that regulators are now actively scrutinising.

MiFID II's conflict of interest requirements, currently under a 2026 ESMA Common Supervisory Action examining how firms comply, apply to any investment firm providing portfolio management services to EU clients. AIFMD II, which required transposition into national law by April 16, 2026, introduces expanded conflict of interest requirements for alternative investment fund managers, including specific rules on delegation arrangements where the delegating manager and the delegate have aligned financial incentives. IOSCO's DeFi Policy Recommendations, published in December 2023 and now being implemented across more than 130 jurisdictions covering 95% of global securities markets, include Recommendation 4, which explicitly requires regulators to mandate the identification and addressing of conflicts of interest in DeFi arrangements.

None of these frameworks were designed with the DeFi vault curator model specifically in mind. All of them, when applied, produce the same requirement: identify the conflict, document it, disclose it, and put in place governance controls that can be demonstrated to regulators. Most current DeFi vault products cannot satisfy that requirement. The regulatory gap is now closing faster than the infrastructure gap.

Three regulatory frameworks converging on the same conclusion: the curator model requires governance infrastructure.

Learnings for Busy Readers

Short on time? Here are the key takeaways. For the full analysis and supporting data, continue reading below.

Three regulatory frameworks are independently converging on the conflict of interest in DeFi vault design.

MiFID II Article 23 requires investment firms to identify, prevent, and manage conflicts of interest when providing investment services. ESMA launched a Common Supervisory Action on MiFID II conflicts of interest compliance in 2026, with a specific focus on remuneration structures and the role of digital platforms in directing investors toward certain products. A vault operator providing portfolio management services to EU clients under a MiFID II license faces direct application of these requirements to its curator incentive structure.

AIFMD II, which required national transposition by April 16, 2026, reinforces that alternative investment fund managers must prevent, or where unavoidable, identify, manage, and monitor conflicts of interest to protect AIF investors. Its expanded delegation rules are directly relevant to the curator-as-operator arrangement: where the delegating manager and the delegate have aligned financial incentives, AIFMD II requires those conflicts to be explicitly managed and disclosed.

IOSCO's Recommendation 4, applying its "same activity, same risk, same regulation" principle to DeFi, requires regulators to mandate that DeFi Responsible Persons proactively identify and resolve conflicts arising from various roles or affiliations. IOSCO specifically identifies the vertical integration of strategy design and execution, the same structural feature that characterises the curator model, as a category of conflict that is not capable of being managed through disclosure alone and may require structural remedies, including legal disaggregation of functions.

For vault operators, the regulatory direction is unambiguous. The curator model, as currently structured, does not satisfy these frameworks without additional governance infrastructure. For institutional allocators, the convergence of these frameworks changes the due diligence question from "does this vault operator have a conflict of interest policy?" to "can they demonstrate that the conflict is structurally managed at the execution level?"

MiFID II: Conflict of Interest Requirements for Investment Firms

MiFID II Article 23 requires investment firms to take all appropriate steps to identify and prevent or manage conflicts of interest between themselves and their clients, and between clients, when providing investment services, including portfolio management. The requirements are not disclosure-only: firms must first prevent conflicts where possible, and where prevention is not possible, manage them through governance controls and disclosure.

The practical requirements under MiFID II include maintaining and operating effective organisational and administrative arrangements to prevent conflicts from adversely affecting client interests, maintaining a conflicts of interest policy that identifies circumstances giving rise to conflicts and specifies procedures to manage those conflicts, and disclosing the general nature and sources of conflicts to clients where organisational arrangements are insufficient to prevent damage to client interests.

The relevance to DeFi vault operators is direct. Any entity providing crypto-asset portfolio management services under a MiFID II license, or under MiCA's CASP framework, which incorporates MiFID II conflict of interest standards by reference, faces the full application of these requirements. A vault operator whose curator function is incentivised by TVL growth and performance fees has a documented conflict between its own economic interests and its clients' interests in mandate-aligned execution. That conflict must be identified in the conflicts of interest policy, managed through governance controls, and disclosed where those controls are insufficient.

The stakes of non-compliance have increased materially in 2026. ESMA launched a Common Supervisory Action on MiFID II conflict of interest requirements, running through 2026, specifically examining how firms comply with their obligations when offering investment products to clients. The supervisory action focuses on the possible impact of staff remuneration and inducements on what products are offered to investors, the role of digital platforms in directing investors toward certain products, and whether firms manage potential conflicts between their own profits and client needs. All three focus areas apply directly to the curator incentive structure in DeFi vault products.

AIFMD II: Delegation, Conflicts, and the Curator-as-Operator Arrangement

AIFMD II, which required national transposition by April 16, 2026, introduces expanded requirements for alternative investment fund managers on delegation, conflicts of interest, and the management of arrangements where the delegating manager and the delegate have aligned financial incentives.

The conflict of interest provisions in AIFMD II are particularly relevant to the DeFi vault context because they address a scenario that maps precisely onto the curator-as-operator arrangement: where a third-party AIFM manages an AIF initially backed by a delegated portfolio manager or a related group entity. In this setup, AIFMD II explicitly acknowledges that potential conflicts of interest are expected and emphasises the need for AIFMs to prevent, or if unavoidable, identify, manage, and monitor these conflicts to protect the interests of the AIF and its investors. (Source: DLA Piper, New AIFMD II Rules on Delegation and Conflicts of Interest, April 2024.)

For institutional allocators that are AIFMs or UCITS management companies, AIFMD II's delegation requirements now extend to the oversight of delegates. An AIFM that delegates portfolio management functions to a third party, including interaction with DeFi vault protocols through a curator, must verify that the delegate complies with AIFMD II standards applicable to those functions. The fact that a delegate is regulated in its home jurisdiction does not relieve the AIFM of this obligation.

The practical implication for DeFi vault allocation is that institutional allocators operating as AIFMs cannot treat the vault operator as a black box. They must verify that the vault operator's governance arrangements for managing curator conflicts of interest satisfy AIFMD II standards, including documentation of the conflict, controls preventing the conflict from adversely affecting allocation decisions, and disclosure to the AIFM that allows it to fulfil its own regulatory obligations.

The institutional digital asset space moves fast. Our subscribers get structured analysis across staking, DeFi vaults, and regulation through DeFi Dispatch, Institutional Lens, DeFi Infrastructure for Institutions, and Legal Layer. No noise. Just the signals that matter. Subscribe to the newsletter at the bottom of this page.

IOSCO Recommendation 4: Conflict of Interest in DeFi at Global Scale

IOSCO's Policy Recommendations for Decentralized Finance, published in December 2023 and now being implemented across jurisdictions covering more than 95% of global securities markets, include Recommendation 4, which requires regulators to mandate that DeFi Responsible Persons proactively identify and resolve conflicts of interest arising from various roles or affiliations.

IOSCO's approach is grounded in its "same activity, same risk, same regulation" principle: DeFi arrangements that provide financial products and services equivalent to those provided by traditional market intermediaries should be regulated to achieve the same outcomes for investor protection and market integrity. Applied to DeFi vault curators, this means that an entity managing assets on behalf of others in a fiduciary-like capacity faces the same conflict of interest requirements as a traditional investment manager, regardless of whether the arrangement is characterised as decentralised.

IOSCO specifically identifies vertical integration of activities and functions as a category of conflict that creates particular regulatory concern. Its Policy Recommendations for Crypto and Digital Asset Markets noted that a CASP engaging in multiple activities in a vertically integrated manner gives rise to conflicts of interest that may not be capable of being managed through disclosure alone and may require structural remedies. (Source: IOSCO, Policy Recommendations for Crypto and Digital Asset Markets, November 2023.) Recommendation 4 for DeFi goes further, urging regulators to consider robust intervention for significant conflicts, including enforcing legal disaggregation and separate registration and regulation of certain activities.

The October 2025 IOSCO thematic review assessing implementation of its crypto and digital asset recommendations found that all participating jurisdictions had made progress implementing Recommendation 2 on governance and disclosure of conflicts of interest, with ten jurisdictions having relevant requirements already in force. The assessment methodology for consistent assessments by IOSCO's Assessment Committee is being developed in 2026, with regular consistency assessments beginning afterwards.

The regulatory direction is visible in how the curator market itself is beginning to evolve. A public report published in December 2025 that analysed the DeFi curator market noted that the curator market currently operates in a regulatory grey area, with curators not holding assets or controlling capital directly but performing work that closely resembles activities of regulated investment advisors. The analysis found that none of the major curators are licensed as of late 2025, but concluded that to serve banks and registered investment advisors, curators will need investment advisor registration, KYC capabilities, and institutional custody integration, the compliance stack that crypto-native players have deliberately avoided.

The same analysis identified the direction of travel explicitly: over the coming years, resolving gaps in regulatory clarity, risk metrics, and technical interoperability will transform curators from crypto-native specialists into a fully licensed, ratings-driven infrastructure that channels institutional capital into on-chain yield with similar standards to traditional finance.

This trajectory is significant for both vault operators and institutional allocators. For vault operators, it signals that the conflict of interest question is not a temporary compliance gap to be managed around. It is a structural feature of the curator model that regulatory frameworks across multiple jurisdictions are independently identified as requiring governance infrastructure. The operators who build that infrastructure now will be positioned as the curator market professionalises. Those who defer it will face a harder transition when licensing requirements arrive.

For institutional allocators, the trajectory creates a timing question. The conflict of interest frameworks that apply to their counterparties today, MiFID II, AIFMD II, and MiCA, already require governance controls that most current vault products do not provide. The IOSCO implementation timeline means that equivalent requirements will apply in an expanding set of jurisdictions. The due diligence question is not whether these requirements will apply. It is whether the vault operators they are considering can satisfy them now.

The Regulatory Trilogy in Summary: Three Requirements, One Missing Layer

This trilogy has traced three distinct regulatory developments, each examining a different dimension of the institutional DeFi compliance environment.

The first article established that MiCA, while not directly regulating DeFi protocols, comprehensively regulates the operators serving institutional clients through them. Its CASP framework introduces mandatory governance standards for conflict of interest management, client asset safeguarding, and audit trail production that apply to any entity providing vault management services to EU clients.

The second article established that Travel Rule enforcement, now applying to every CASP-to-CASP transfer with no minimum threshold in the EU since December 30, 2024, creates a structural compliance gap in DeFi vault architecture. Smart contracts do not generate originator and beneficiary data. Closing the gap requires a data layer above the execution environment that most vault products were never designed to include.

This article establishes that conflict of interest frameworks across MiFID II, AIFMD II, and IOSCO's DeFi recommendations are independently converging on the curator model as a compliance problem. The vertical integration of strategy design, execution, and economic benefit without independent oversight creates conflicts that these frameworks require to be identified, documented, disclosed, and managed through governance controls that can be demonstrated to regulators.

All three regulatory developments point to the same missing infrastructure layer: an independent governance function sitting above the execution environment, operating at the transaction level, independent of the curator, validating mandate alignment, producing an exportable compliance log, and maintaining contractually defined role separation. The first trilogy of this series established that this layer is missing from most DeFi vault products. This trilogy establishes that its absence is now a regulatory compliance problem across three distinct and converging frameworks.

Key Takeaway

Conflict-of-interest regulation did not arrive in DeFi. It was already there, in MiFID II and AIFMD, applied to the investment managers and fund operators who are the institutional allocators in DeFi vault products. What has changed is that AIFMD II has now extended those requirements to delegation arrangements, MiCA has applied equivalent standards to vault operators directly, and IOSCO's DeFi recommendations are extending the same framework globally across 95% of securities markets.

The curator model, as currently structured in most DeFi vault products, does not satisfy these frameworks without additional governance infrastructure. The conflict between curator incentives and institutional mandate alignment must be identified, documented, disclosed, and managed through controls that can be demonstrated to regulators. Most current products cannot produce that demonstration.

For vault operators, the direction is clear. The regulatory frameworks that govern their institutional clients are already applying conflict of interest requirements that reach into the vault architecture. The operators who build independent governance infrastructure now will be positioned for the institutional market as it matures. Those who treat conflict of interest management as a future compliance question will find it has already become a present one.

For institutional allocators, the two trilogies of this series have traced a complete picture: the structural gaps in DeFi vault architecture, the conflict of interest at the curator layer, the mandate validation standard that closes both gaps, and now the regulatory frameworks that make building that governance layer a legal requirement rather than a best practice.

The infrastructure that satisfies all three regulatory frameworks, pre-execution controls, exportable compliance logs, and contractual role separation, is the same infrastructure that the first trilogy identified as the missing governance layer in DeFi vault design. The regulatory environment is not creating a new requirement. It is formalising the one that was always there.

The DeFi Infrastructure for Institutions series continues. The next sequence examines specific dimensions of how the protection layer operates in practice for specific institutional profiles.

Frequently Asked Questions (FAQs)

How does MiFID II's conflict of interest framework apply to DeFi vault operators?

MiFID II Article 23 requires investment firms providing portfolio management services to identify, prevent, and manage conflicts of interest between themselves and their clients. Any vault operator providing crypto-asset portfolio management services under a MiFID II license, or under MiCA's CASP framework, which incorporates MiFID II conflict of interest standards by reference, faces direct application of these requirements. A curator incentivised by TVL growth and performance fees has a documented conflict between its economic interests and its clients' interests in mandate-aligned execution. That conflict must be identified in the operator's conflicts of interest policy, managed through governance controls, and disclosed where those controls are insufficient to prevent damage to client interests.

What does AIFMD II add to the conflict of interest requirements for institutional allocators?

AIFMD II, which required national transposition by April 16, 2026, expands conflict of interest requirements for alternative investment fund managers and introduces specific obligations around delegation arrangements. An AIFM that delegates portfolio management functions to a third party, including interaction with DeFi vault protocols through a curator, must verify that the delegate complies with AIFMD II standards applicable to those functions. The fact that a delegate is regulated in its home jurisdiction does not relieve the AIFM of this obligation. Institutional allocators operating as AIFMs must verify that vault operators' governance arrangements for managing curator conflicts satisfy AIFMD II standards, not just that the operator holds a relevant license.

What is IOSCO Recommendation 4, and why does it matter for DeFi vault design?

IOSCO Recommendation 4 from its December 2023 DeFi Policy Recommendations requires regulators to mandate that DeFi Responsible Persons proactively identify and resolve conflicts of interest arising from various roles or affiliations. IOSCO applies its "same activity, same risk, same regulation" principle to DeFi: arrangements providing financial services equivalent to traditional intermediaries face the same conflict of interest requirements. IOSCO specifically identifies vertical integration of strategy design and execution as a category of conflict that may not be manageable through disclosure alone and may require structural remedies, including legal disaggregation of functions. With implementation progressing across jurisdictions covering 95% of global securities markets, this recommendation is creating compliance obligations in an expanding set of regulatory frameworks.

What does the ESMA Common Supervisory Action on MiFID II conflicts of interest mean in practice?

ESMA launched a Common Supervisory Action on MiFID II conflict of interest compliance in 2026, running through the year across national competent authorities in EU member states. The action specifically examines remuneration structures and their impact on product recommendations, the role of digital platforms in directing investors toward certain products, and whether firms manage conflicts between their own profits and client needs. All three focus areas apply directly to curator incentive structures in DeFi vault products. Firms under supervisory scrutiny that cannot demonstrate governance controls for these conflicts face regulatory action ranging from supervisory guidance to enforcement.

P2P.org builds the protection layer that sits between regulated institutions and DeFi execution environments, independently of the curators who manage allocation strategies. If you are evaluating the infrastructure requirements for a DeFi allocation program, talk to our team.

Disclaimer This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or investment advice. Regulatory obligations may vary depending on jurisdiction and specific business activities. Readers should consult their own legal and compliance advisors regarding applicable requirements.

Subscribe to P2P-economy

Get the latest posts delivered right to your inbox

<hr><h2 id="series-institutional-lens-validation-infrastructure"><strong>Series:</strong> Institutional Lens | Validation Infrastructure</h2><p>The Institutional Lens series unpacks the protocol mechanics, infrastructure decisions, and governance considerations that matter most for institutional participants in proof-of-stake networks. Each article is written for professionals operating at the intersection of traditional finance and blockchain infrastructure, including digital asset custodians, crypto-native funds, ETF issuers, treasury teams, and staking product managers.</p><p><strong>Previously in the series:</strong></p><ul><li><a href="https://p2p.org/economy/why-institutional-capital-needs-a-protection-layer-in-proof-of-stake-networks/">Why Institutional Capital Needs a Protection Layer in Proof-of-Stake Networks</a></li><li><a href="https://p2p.org/economy/solana-staking-for-institutions-native-vs-liquid-a-decision-framework/">Solana Staking for Institutions: Native vs. Liquid. A Decision Framework.</a></li></ul><h2 id="learnings-for-busy-readers">Learnings for Busy Readers</h2><p>The previous two articles in this series established the case for a protection layer in proof-of-stake networks and the specific decision framework for Solana. This article moves one level up: from single-network decisions to full institutional staking program design.</p><p>What you will find below is not a yield comparison. It is a program architecture framework.</p><p>The core argument is this: most institutions entered proof-of-stake through a single network, usually Ethereum, because that was the only one with an unambiguous legal status in the United States. The March 17, 2026, SEC and CFTC joint interpretation changed that. Sixteen assets are now classified as digital commodities, including SOL, ADA, and DOT. The legal basis that restricted most compliance teams to Ethereum-only programs is gone.</p><p>What remains is a program design problem. Multi-network institutional staking programs are structurally different from single-network ones. Each network has its own unbonding timeline, reward mechanics, slashing conditions, governance obligations, and reporting requirements. A program that treats each network as an isolated position will accumulate operational fragmentation, compliance gaps, and unmodeled liquidity risk.</p><p>This article explains how to design the program correctly from the start.</p><h2 id="who-this-article-is-for">Who This Article Is For</h2><p>This guide is written for professionals building or governing multi-network staking programs at an institutional scale, including:</p><ul><li>Digital asset custodians evaluating program expansion beyond Ethereum</li><li>Crypto-native hedge funds and asset managers are adding PoS assets to mandates</li><li>ETF and ETP issuers with staking-integrated products across multiple networks</li><li>Treasury teams holding Ethereum, Solana, and other newly classified commodities</li><li>Staking product managers designing validator programs for institutional clients</li><li>Infrastructure engineers responsible for multi-network validator operations</li><li>Validator risk committees reviewing program architecture and provider relationships</li></ul><p><a href="http://p2p.org/?ref=p2p.org">P2P.org</a> operates non-custodial validator infrastructure in a client-controlled architecture aligned with protocol rules across more than 40 proof-of-stake networks.</p><h2 id="why-single-network-programs-no-longer-match-the-market">Why Single-Network Programs No Longer Match the Market</h2><p>Until March 2026, most institutional staking programs were built on a single-network foundation. Ethereum was the default because it carried the clearest regulatory posture in the United States. SOL, ADA, DOT, and other proof-of-stake assets remained either restricted or unaddressed in most institutional mandates, not because of operational concerns, but because of legal uncertainty.</p><p>The March 17, 2026, SEC and CFTC joint interpretation removed that uncertainty. The ruling explicitly confirmed that protocol staking across solo, self-custodial, custodial, and liquid models does not constitute a securities transaction for any of the 16 named digital commodities. SOL, ADA, DOT, XRP, and others are now classified as digital commodities with a staking posture that compliance departments can support without securities risk concerns (Source: <a href="https://phemex.com/blogs/sec-ruling-crypto-etfs-staking?ref=p2p.org">Phemex</a>).</p><p>At the same time, institutional capital has moved:</p><ul><li>Ethereum's staking ratio reached a record 31.1% of total supply in March 2026</li><li>Solana ETFs passed $1 billion in cumulative inflows in early March 2026, with Goldman Sachs disclosing $108 million in SOL ETF holdings as of April 2026</li><li>BlackRock's ETHB, the first staking-integrated ETF from a major asset manager, debuted at $107 million and reached approximately $254 million in AUM within its first week</li><li>DOT's unbonding period was reduced from 28 days to 24 to 48 hours in March 2026, materially changing the liquidity profile of Polkadot staking for institutions</li></ul><p>The market is now structurally multi-network. Institutions that design their staking programs as single-network operations are leaving addressable exposure unmanaged and, in many cases, accepting dilution on proof-of-stake assets they already hold but are not staking (Source: <a href="https://coinlaw.io/cryptocurrency-staking-statistics/?ref=p2p.org">CoinLaw</a>).</p><h2 id="the-four-dimensions-of-multi-network-program-design">The Four Dimensions of Multi-Network Program Design</h2><p>A well-designed institutional staking program across multiple networks requires explicit decisions across four dimensions: liquidity architecture, risk layering, reporting infrastructure, and governance policy. Each dimension behaves differently network by network, and all four must be designed at the program level before capital is allocated at the network level.</p><h3 id="dimension-1-liquidity-architecture">Dimension 1: Liquidity Architecture</h3><p>The most underappreciated element of multi-network staking programs is liquidity. Each proof-of-stake network imposes its own unbonding timeline, and those timelines are not aligned with each other or with the liquidity frameworks institutions typically apply to other asset classes.</p><p>As of May 2026, the relevant unbonding parameters for the networks most commonly included in institutional programs are:</p><p><strong>Ethereum:</strong> Variable withdrawal queue. Under normal conditions, exit processing takes one to five days. During periods of elevated exit demand, such as the September 2025 peak where 2.67 million ETH was queued and wait times exceeded 46 days, the timeline can extend materially. The queue is always dynamic and must be monitored in real time. (Source: <a href="https://www.validatorqueue.com/?ref=p2p.org">ValidatorQueue.com</a>)</p><p><strong>Solana:</strong> Approximately two to three days under standard conditions. The epoch structure means unstaking initiated at the start of an epoch completes at the end of the following epoch, creating a predictable but not instant exit timeline.</p><p><strong>Polkadot:</strong> Reduced to 24 to 48 hours as of March 2026, down from 28 days. This is a material change that significantly improves Polkadot's liquidity profile for institutional programs. (Source: <a href="https://cryptoyieldguide.com/blog/staking-rewards-comparison-2026/?ref=p2p.org">Passive Yield Lab</a>)</p><p><strong>Cosmos (ATOM):</strong> 21-day unbonding period. This remains among the longest lock-ups in the institutional PoS landscape and requires specific liquidity planning.</p><p><strong>Cardano (ADA):</strong> No lock-up period. Staked ADA can be spent or transferred at any time without unstaking. This is structurally unusual and gives ADA a liquidity profile closer to an unencumbered holding than a locked position.</p><p>The institutional implication is that multi-network programs should be designed around a liquidity ladder: an allocation framework that distributes staking exposure across networks with different unbonding characteristics, so that the program as a whole maintains liquidity at predictable points even when individual positions are in unbonding.</p><p>A liquidity ladder for a multi-network program might distribute exposure across three tiers:</p><p><strong>Tier 1: Liquid or near-liquid positions.</strong> ADA (no lock-up) and liquid staking token positions where the LST can be swapped near-instantly. These provide the program's liquidity buffer.</p><p><strong>Tier 2: Short-horizon positions.</strong> SOL (two to three days), ETH under normal queue conditions (one to five days), and DOT post-March 2026 (24 to 48 hours). These positions can be exited within a standard institutional settlement window under normal market conditions.</p><p><strong>Tier 3: Long-horizon positions.</strong> ATOM (21 days) and any other network with extended unbonding periods. These positions should be sized to the portion of the allocation that the institution can treat as genuinely illiquid over the unbonding window.</p><p>Portfolio managers, custodians, and treasury teams with redemption obligations should integrate these tiers into position sizing before allocating, not after.</p><figure class="kg-card kg-image-card kg-card-hascaption"><img src="https://p2p.org/economy/content/images/2026/05/multi-network-institutional-staking-program-matrix.jpg" class="kg-image" alt="A structured comparison table or matrix layout, not a flowchart. The visual should communicate at a glance that different networks require different institutional treatment across the same set of variables." loading="lazy" width="1600" height="900" srcset="https://p2p.org/economy/content/images/size/w600/2026/05/multi-network-institutional-staking-program-matrix.jpg 600w, https://p2p.org/economy/content/images/size/w1000/2026/05/multi-network-institutional-staking-program-matrix.jpg 1000w, https://p2p.org/economy/content/images/2026/05/multi-network-institutional-staking-program-matrix.jpg 1600w" sizes="(min-width: 720px) 720px"><figcaption><i><em class="italic" style="white-space: pre-wrap;">Multi-Network Institutional Staking Program Framework</em></i></figcaption></figure><h3 id="dimension-2-risk-layering">Dimension 2: Risk Layering</h3><p>Single-network staking programs carry one set of protocol risks. Multi-network programs carry multiple sets, and those sets do not behave the same way. Designing a multi-network program without mapping risk by network is equivalent to building a fixed-income portfolio without distinguishing credit qualities.</p><p>The relevant risk categories at the network level are:</p><p><strong>Slashing risk:</strong> Slashing conditions, triggers, and penalty magnitudes differ by network. On Ethereum, slashing is triggered by double-signing and surrounding votes, with a correlation multiplier that amplifies penalties when multiple validators are slashed simultaneously. On Solana, slashing is currently not implemented at the base layer, though this may change as the network matures. On Polkadot, the Nominated Proof-of-Stake model introduces slashing for both validators and their nominators, meaning institutional allocators who nominate a validator share in any slash applied to that validator. These distinctions require network-specific slashing risk policies.</p><p><strong>Concentration risk:</strong> Institutions allocating to multiple networks through a single infrastructure provider face correlated operational risk if that provider uses homogeneous infrastructure across networks. An operational failure that affects the provider's shared signing or monitoring systems could impact positions across all supported networks simultaneously. Multi-network programs should evaluate whether their infrastructure provider maintains operationally independent systems by network or uses shared architecture.</p><p><strong>Validator concentration risk on the network:</strong> On Solana, the active validator count dropped from approximately 2,500 to under 800 in 2026, raising network-level concentration concerns. When a network's validator set is concentrated, institutional delegators who choose poorly distributed validators amplify that concentration rather than mitigate it. Delegation strategy must account for network-level validator health, not just individual validator quality.</p><p><strong>Protocol upgrade risk:</strong> Each network has its own upgrade cadence and governance process. A staking program spanning five networks must account for the fact that protocol upgrades on any of those networks may affect slashing conditions, reward mechanics, or unbonding parameters, often with short notice. Institutions that do not monitor governance across their full network portfolio will be surprised by material changes, as they would have been by Polkadot's unbonding reduction in March 2026.</p><h3 id="dimension-3-reporting-infrastructure">Dimension 3: Reporting Infrastructure</h3><p>Single-network staking programs can often be managed with network-specific reporting tools. Multi-network programs cannot. The operational cost of maintaining five or more separate reporting stacks, each with different data formats, epoch timings, and reward calculation methodologies, grows rapidly and introduces reconciliation risk that compliance and audit teams cannot absorb at scale.</p><p>Institutional-grade multi-network reporting requires:</p><p><strong>Reward attribution at the validator level, by epoch, for every supported network.</strong> A consolidated view is useful for treasury oversight. An audit-ready record must be disaggregated by network, validator, and period.</p><p><strong>Unified reward classification.</strong> Different networks produce rewards from different sources: base protocol issuance, transaction fees, and MEV-equivalent mechanisms. Multi-network reporting must classify reward types consistently across networks so that accounting teams can apply appropriate treatment under applicable standards.</p><p><strong>Unbonding and exit event tracking.</strong> A program spanning multiple networks will have validators entering and exiting the unbonding process continuously. Reporting infrastructure must capture these events with timestamps for audit and reconciliation purposes.</p><p><strong>Network-specific slashing event logging.</strong> Any slashing event, regardless of network, must be captured with root cause, timestamp, and amount for regulatory disclosure purposes where applicable.</p><p><strong>Format compatibility with institutional back-office systems.</strong> Reward data that cannot be ingested by the institution's existing accounting, risk management, or custody platform creates manual reconciliation work that scales with program size.</p><p>Institutions evaluating infrastructure providers for multi-network programs should request sample reporting packs for every network in their target allocation, not just for Ethereum. The quality gap between providers on reporting is often more significant on smaller networks than on Ethereum, where baseline tooling is well established.</p><h3 id="dimension-4-governance-policy">Dimension 4: Governance Policy</h3><p>In single-network Ethereum programs, governance participation is often treated as a secondary consideration. In multi-network programs, it becomes a first-order governance obligation.</p><p>Every proof-of-stake network where an institution holds staked assets has governance processes. Protocol upgrades, parameter changes, reward rate adjustments, and slashing condition modifications are all governed through validator and delegator participation. When an institution delegates to a validator, it delegates governance representation to that validator. For regulated entities with fiduciary obligations, this is not a passive decision.</p><p>A multi-network institutional staking program requires a documented governance participation policy that addresses:</p><p><strong>Which networks have material governance decisions pending or expected?</strong> Not all networks are equally active in governance. Ethereum governance is slow and deliberate. Cosmos governance is more frequent. Polkadot's OpenGov model enables continuous on-chain voting. Programs must identify which networks require active governance tracking.</p><p><strong>How the institution's delegation choices affect governance representation?</strong> On Cosmos, delegators vote independently of their validators. On Ethereum, validators vote on behalf of their stake in protocol upgrade decisions. These models produce different governance obligations and different levels of delegation accountability.</p><p><strong>What is the institution's policy on protocol upgrade participation?</strong> This includes whether the institution has a formal position on contentious upgrades, whether it delegates governance decisions entirely to the validator, and what the escalation path is when a validator votes against the institution's interests.</p><p><strong>How governance participation is documented?</strong> For custodians managing staked assets on behalf of clients, governance documentation is an extension of fiduciary record-keeping. For ETF issuers, governance decisions on staked assets may eventually carry disclosure obligations.</p><h2 id="the-program-level-due-diligence-checklist">The Program-Level Due Diligence Checklist</h2><p>For staking product managers, validator risk committees, and compliance teams building or reviewing a multi-network institutional staking program.</p><h3 id="liquidity-architecture">Liquidity architecture</h3><ul><li>[ ] Has a liquidity tier analysis been completed for every network in the program?</li><li>[ ] Is the liquidity ladder documented and integrated into position sizing?</li><li>[ ] Are unbonding timelines current and verified at the network level, including any recent parameter changes?</li><li>[ ] Is exit queue monitoring in place for Ethereum and any other networks with variable queues?</li><li>[ ] Are redemption obligations, fund liquidity covenants, or treasury mandates mapped against the worst-case unbonding scenario for each network?</li></ul><h3 id="risk-layering">Risk layering</h3><ul><li>[ ] Is there a network-specific slashing risk policy for every network in the program?</li><li>[ ] Is the program's infrastructure provider evaluated for correlated operational risk across networks?</li><li>[ ] Is validator concentration risk assessed at the network level for each delegation?</li><li>[ ] Is there a protocol governance monitoring process that covers all networks in scope?</li><li>[ ] Are tail risk scenarios (correlated slashing, simultaneous exit queue events) modelled at the program level?</li></ul><h3 id="reporting-infrastructure">Reporting infrastructure</h3><ul><li>[ ] Can the infrastructure provider deliver validator-level, epoch-level reward attribution for every network in scope?</li><li>[ ] Is reward classification consistent and documented across networks for accounting purposes?</li><li>[ ] Are exit, unbonding, and slashing events logged with timestamps compatible with audit requirements?</li><li>[ ] Is reporting output compatible with the institution's back-office systems for all supported networks?</li><li>[ ] Has a sample reporting pack been reviewed for each network in the target allocation?</li></ul><h3 id="governance-policy">Governance policy</h3><ul><li>[ ] Is there a documented governance participation policy covering every network in the program?</li><li>[ ] Is the policy reviewed and updated following material protocol upgrades or governance parameter changes?</li><li>[ ] Are delegation decisions evaluated for their governance implications, not just their operational quality?</li><li>[ ] For regulated entities: is there a process for documenting governance decisions for fiduciary record-keeping purposes?</li></ul><h2 id="evaluating-infrastructure-providers-for-multi-network-programs">Evaluating Infrastructure Providers for Multi-Network Programs</h2><p>The selection criteria for a validator infrastructure provider shift materially when the program spans multiple networks. Single-network evaluations can focus deeply on one protocol. Multi-network evaluations must assess depth, consistency, and integration across every network in scope.</p><p>Key questions for multi-network program evaluation:</p><p>What is the provider's operational track record on each specific network in the target allocation? Depth on Ethereum does not imply depth on Polkadot or Cosmos. Request network-specific incident history and performance data.</p><p>Are the infrastructure, key management, and slashing protection controls operationally consistent across networks, or does the provider use different architectures and standards per network?</p><p>Can the provider deliver consolidated reporting that covers every network in the program within a single integrated system, or will reporting require separate per-network integrations?</p><p>Does the provider monitor protocol governance across all supported networks, and how does it communicate material governance developments to institutional clients?</p><p><a href="http://p2p.org/?ref=p2p.org">P2P.org</a> supports non-custodial validator infrastructure across more than 40 proof-of-stake networks, with consistent operational standards and validator-level reporting across each. Infrastructure details and integration documentation for institutional programs are available at <a href="https://p2p.org/staking?ref=p2p.org">p2p.org/staking</a> and <a href="https://p2p.org/networks/ethereum-staking-service?ref=p2p.org">p2p.org/networks</a>. For multi-network reporting and institutional integration architecture, see <a href="https://docs.p2p.org/?ref=p2p.org">docs.p2p.org</a>.</p><p>For the foundational institutional staking due diligence framework, including the seven dimensions of validator evaluation that apply across all networks, see the Validator Playbook series article: <a href="https://p2p.org/economy/validator-due-diligence-framework-what-institutions-really-need-to-evaluate/">Validator Due Diligence Framework: What Institutions Really Need to Evaluate</a>.</p><div class="kg-card kg-callout-card kg-callout-card-grey"><div class="kg-callout-text"><b><strong style="white-space: pre-wrap;">The institutional digital asset space moves fast.</strong></b> Our subscribers get structured analysis across staking, DeFi vaults, and regulation through <i><em class="italic" style="white-space: pre-wrap;">DeFi Dispatch</em></i>, <i><em class="italic" style="white-space: pre-wrap;">Institutional Lens</em></i>, <i><em class="italic" style="white-space: pre-wrap;">DeFi Infrastructure for Institutions</em></i>, and <i><em class="italic" style="white-space: pre-wrap;">Legal Layer</em></i>. No noise. Just the signals that matter. <b><strong style="white-space: pre-wrap;">Subscribe to the newsletter at the bottom of this page.</strong></b></div></div><h2 id="key-takeaway-for-custodians-funds-etf-issuers-and-treasury-teams">Key Takeaway for Custodians, Funds, ETF Issuers, and Treasury Teams</h2><p>The March 2026 regulatory shift did not just expand the universe of assets available for institutional staking. It exposed a program design gap that most institutions have not yet addressed.</p><p>Single-network staking programs were built for a single-network regulatory world. That world is gone. Institutions holding Ethereum, Solana, Polkadot, Cosmos, and Cardano across their portfolios now have the legal basis, the infrastructure, and the market context to build multi-network programs. The question is whether the program architecture can support that expansion without accumulating unmodeled liquidity risk, fragmented reporting, and undocumented governance obligations.</p><p>The four dimensions covered in this article, including liquidity architecture, risk layering, reporting infrastructure, and governance policy, are not independent checklists. They are interdependent elements of a program-level design decision. Institutions that address them together before allocating across networks will operate with the same discipline they apply to every other multi-asset program. Institutions that treat each network as a standalone position will eventually encounter the integration failures that come with fragmented program design.</p><p>Protocol-generated rewards are determined by network conditions and are variable. <a href="http://p2p.org/?ref=p2p.org">P2P.org</a> does not control or set reward rates. Slashing risks are protocol-defined and client-borne. Operational safeguards are implemented to reduce slashing exposure, but do not eliminate protocol-level risk.</p><h2 id="frequently-asked-questions-faqs">Frequently Asked Questions (FAQs)<br></h2><h3 id="what-is-an-institutional-staking-program">What is an institutional staking program?</h3><p>An institutional staking program is the structured approach through which a regulated organization (a custodian, fund, ETF issuer, or treasury team) participates in proof-of-stake consensus across one or more blockchain networks. Unlike retail staking, an institutional staking program requires deliberate design across custody architecture, risk management, liquidity planning, reward reporting, and governance policy. At the multi-network level, it also requires a framework that accounts for the different mechanics, timelines, and obligations of each network in scope.</p><h3 id="why-does-the-march-2026-sec-and-cftc-ruling-matter-for-multi-network-staking-programs">Why does the March 2026 SEC and CFTC ruling matter for multi-network staking programs?</h3><p>The ruling explicitly confirmed that protocol staking across all four models, including solo, self-custodial, custodial, and liquid, does not constitute a securities transaction for any of the 16 named digital commodities, including SOL, ADA, DOT, and XRP. This removed the primary legal basis that had restricted most institutional compliance teams to Ethereum-only staking programs. Institutions can now build multi-network programs across the full set of named commodities without the securities risk concern that previously limited them.</p><h3 id="what-is-a-liquidity-ladder-in-the-context-of-an-institutional-staking-program">What is a liquidity ladder in the context of an institutional staking program?</h3><p>A liquidity ladder is an allocation framework that distributes staking exposure across networks with different unbonding timelines, so that the program as a whole maintains liquidity at predictable points even when individual positions are in unbonding. Tier 1 positions use networks with no lock-up or near-instant exit (ADA, LST positions). Tier 2 positions use networks with short unbonding periods (SOL, DOT post-March 2026, ETH under normal queue conditions). Tier 3 positions use networks with longer unbonding periods (ATOM at 21 days). Position sizing in each tier should be calibrated against the institution's redemption obligations and liquidity covenants.</p><h3 id="how-do-unbonding-timelines-differ-across-the-main-proof-of-stake-networks-in-2026">How do unbonding timelines differ across the main proof-of-stake networks in 2026?</h3><p>As of May 2026, Cardano has no lock-up. Polkadot reduced its unbonding period to 24 to 48 hours in March 2026, down from 28 days. Solana requires approximately two to three days. Ethereum has a variable withdrawal queue that takes one to five days under normal conditions, but extended beyond 46 days during the September 2025 exit queue peak. Cosmos requires a 21-day unbonding period. These differences are material for liquidity planning and must be integrated into position sizing before capital is allocated.</p><h3 id="how-does-polkadots-nominated-proof-of-stake-model-create-different-slashing-exposure-than-ethereum">How does Polkadot's Nominated Proof-of-Stake model create different slashing exposure than Ethereum?</h3><p>On Polkadot, slashing penalties apply to both the validator and its nominators in proportion to their stake. This means institutional allocators who nominate a validator share in any slash applied to that validator. On Ethereum, slashing penalties apply to the validator's own stake and do not directly reduce delegator balances. Institutions entering Polkadot staking must account for this structural difference in their slashing risk policy and in the due diligence they apply to validator selection.</p><h3 id="what-should-institutional-reporting-look-like-for-a-multi-network-staking-program">What should institutional reporting look like for a multi-network staking program?</h3><p>Institutional reporting for a multi-network program should provide validator-level, epoch-level reward attribution for every network in the program, with consistent reward classification across networks for accounting treatment, timestamped logging of all exit, unbonding, and slashing events, and output formats compatible with the institution's existing back-office systems. Consolidated reporting that spans all networks in a single integrated system is preferable to per-network reporting stacks that require manual reconciliation.</p><h3 id="what-governance-obligations-does-a-multi-network-staking-program-create">What governance obligations does a multi-network staking program create?</h3><p>Every proof-of-stake network in a multi-network program has governance processes. Protocol upgrades, reward parameter changes, and slashing condition modifications are all governed through validator and delegator participation. When an institution delegates to a validator, it delegates governance representation to that validator. Regulated entities with fiduciary obligations should maintain a documented governance participation policy covering all networks in scope, including how delegation choices affect governance representation, how protocol upgrades are evaluated, and how governance decisions are logged for fiduciary record-keeping purposes.</p><hr><h2 id="about-p2porg">About P2P.org</h2><p><a href="http://p2p.org/?ref=p2p.org">P2P.org</a> builds the protection layer that sits between regulated institutions and DeFi execution environments, independently of the curators who manage allocation strategies. If you are evaluating the infrastructure requirements for a DeFi allocation program, <a href="https://p2p.org/?ref=p2p.org#form">talk to our team</a>.</p><hr><h3 id="disclaimer">Disclaimer</h3><p>This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or investment advice. Regulatory obligations may vary depending on jurisdiction and specific business activities. Readers should consult their own legal and compliance advisors regarding applicable requirements.</p>

<hr><h2 id="series-defi-dispatch">Series: DeFi Dispatch</h2><p>DeFi Dispatch is <a href="http://p2p.org/?ref=p2p.org">P2P.org</a>'s twice-monthly roundup of DeFi developments for institutional participants. Each edition covers the signals that matter for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams operating at the intersection of traditional and on-chain finance.</p><p>👉 Subscribe to our newsletter at the bottom of this page to receive a monthly summary of the latest DeFi and staking developments, curated for institutional participants.</p><p>Missed the previous edition? Catch up here: <a href="https://p2p.org/economy/defi-dispatch-defi-news-april-2026-issue-2/">DeFi Dispatch: DeFi News and Signals April 2026 (Issue 2)</a></p><h2 id="quick-learnings-for-busy-readers">Quick Learnings for Busy Readers</h2><p>Short on time? Here are the key takeaways. For the full analysis, continue reading below.</p><p>The first half of May brought five developments that institutional participants in DeFi and staking infrastructure should track closely.</p><ul><li>A Federal Reserve Governor formally confirmed that U.S. tokenized assets have more than doubled to $25 billion, placing validator and protocol reliability inside the Fed's financial stability assessment framework for the first time.</li><li>Anchorage Digital and J.P. Morgan Asset Management announced a yield-bearing stablecoin reserve model on Solana, embedding proof-of-stake validator infrastructure directly into institutional stablecoin reserve management.</li><li>Solana staking ETFs crossed $1 billion in cumulative net inflows, with demand remaining positive even during periods of negative price performance, signalling institutional capital is allocating based on infrastructure conviction rather than short-term price momentum.</li><li>OpenTrade raised $17 million with participation from a16z Crypto to expand its stablecoin yield infrastructure backed by real-world assets, as the $310 billion stablecoin market drives structural demand for compliant, diversified yield strategies.</li><li>Tokenized private credit approached $18 billion in active on-chain deployment, with analysts projecting $40 billion by year-end as traditional finance private credit managers follow Apollo's governance-heavy DeFi protocol partnership model.</li></ul><h2 id="story-1-federal-reserve-governor-cook-confirms-us-tokenized-assets-have-doubled-to-25-billion">Story 1: Federal Reserve Governor Cook Confirms U.S. Tokenized Assets Have Doubled to $25 Billion</h2><p>Federal Reserve Governor Lisa Cook delivered a landmark speech on tokenization at the Central Bank of West African States Conference in Dakar on May 8, confirming that tokenized assets in the U.S. have more than doubled in market capitalization over the past year, reaching approximately $25 billion. Cook identified collateral and liquidity management as the primary institutional use case driving adoption, pointing to the intersection of large existing markets, including bonds, money market fund shares, and repurchase agreements, with opportunities for new functionality through automation and programmability.</p><p>Cook explicitly flagged smart contract and DeFi vulnerabilities as risks that could leave less room for human intervention when errors or attacks occur, placing validator and protocol reliability inside the Fed's systemic risk vocabulary for the first time. She also confirmed that the Federal Reserve is actively researching tokenization's implications and engaging with international organizations, peer central banks, and industry participants to monitor responsible innovation.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>A sitting Fed Governor formally framing blockchain infrastructure reliability as a financial stability consideration signals that supervisory expectations for validator and protocol operations are beginning to converge with those applied to traditional market infrastructure</li><li>Cook's identification of repo and collateral management as the primary tokenization use cases maps directly onto the on-chain settlement infrastructure already being built on Ethereum and Solana</li><li>For custodians and staking teams, the Fed's active engagement means operational standards for blockchain infrastructure are increasingly likely to be subject to formal supervisory expectations, not only market convention</li></ul><p>Source: <a href="https://finadium.com/feds-cook-says-collateral-and-liquidity-management-is-the-major-tokenization-use-case/?ref=p2p.org" rel="noreferrer">Federal Reserve Board, Finadium, May 2026</a>.</p><h2 id="story-2-anchorage-digital-and-jp-morgan-build-yield-bearing-stablecoin-reserves-on-solana">Story 2: Anchorage Digital and J.P. Morgan Build Yield-Bearing Stablecoin Reserves on Solana</h2><p>Anchorage Digital announced a cashless stablecoin reserve model on Solana on May 5, working with J.P. Morgan Asset Management to develop a tokenized instrument solution powering the liquidity framework. Rather than holding static cash buffers, the model holds reserves in yield-bearing, low-risk tokenized instruments on Solana that can generate on-demand liquidity, with Anchorage Digital issuing and managing stablecoins on behalf of institutional partners under this structure.</p><p>Anchorage Digital already serves as the regulated custodian for Tether's U.S. stablecoin, Ethena's stablecoin, Western Union's stablecoin, and BlackRock's BUIDL. Every architecture decision it makes about where reserve assets are held carries ecosystem-wide implications for which blockchain networks attract institutional reserve capital.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-1">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>Yield-bearing stablecoin reserves on a proof-of-stake network require that network to operate with institutional-grade uptime and performance, making Solana validator infrastructure part of the reserve management stack</li><li>J.P. Morgan Asset Management's involvement signals that the largest traditional asset managers are now actively designing the tokenized instrument layer that will sit inside stablecoin reserve structures</li><li>For staking product managers and validator operators, this announcement represents the clearest signal yet that institutional stablecoin infrastructure and proof-of-stake network participation are converging into a single operational layer</li></ul><p>Source: <a href="https://www.pymnts.com/cryptocurrency/2026/anchorage-digital-pursues-more-efficient-institutional-stablecoin-liquidity/?ref=p2p.org" rel="noreferrer">Anchorage Digital, PYMNTS, May 2026</a>.</p><h2 id="story-3-solana-staking-etfs-cross-1-billion-in-cumulative-net-inflows">Story 3: Solana Staking ETFs Cross $1 Billion in Cumulative Net Inflows</h2><p>SOL spot ETFs recorded a net inflow of $21.3 million on May 6, with the Bitwise Solana Staking ETF leading at $20.77 million in single-day inflows and bringing its total assets to $850 million. Historical cumulative net inflows across all SOL spot ETFs crossed $1.044 billion, with Bitwise alone recording $8.5 billion in cumulative historical net inflows since launch.</p><p>Solana staking ETF inflows have remained positive despite negative price performance for SOL over several months, a pattern that decouples from conventional risk-on and risk-off behaviour in crypto markets. The Fidelity Solana Fund ETF fee waiver expires May 18, after which a 0.25% expense ratio and 15% staking fee apply, making this an important test of whether institutional demand sustains once full fee loads are introduced.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-2">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>Inflows remaining positive through price drawdowns signal institutional capital is allocating based on infrastructure conviction rather than short-term price momentum, a more durable demand driver for validator infrastructure</li><li>The fee competition among Bitwise, Fidelity, and Grayscale establishes the economic reference points that will govern how validator infrastructure is priced within regulated product wrappers</li><li>Crossing $1 billion in cumulative inflows confirms that staking-enabled ETF products have found sustained institutional demand beyond the launch window</li></ul><p>Source: <a href="https://coin360.com/news/fidelity-solana-staking-etf-launch-institutional-shift?ref=p2p.org" rel="noreferrer">SoSoValue via KuCoin, Coin360, Solana Compass, May 2026</a>.</p><h2 id="story-4-opentrade-raises-17-million-to-expand-stablecoin-yield-infrastructure-backed-by-real-world-assets">Story 4: OpenTrade Raises $17 Million to Expand Stablecoin Yield Infrastructure Backed by Real-World Assets</h2><p>Stablecoin infrastructure platform OpenTrade raised $17 million on May 6 in a round led by Mercury Fund and Notion Capital, with participation from a16z Crypto, bringing its total funding to more than $30 million. The firm enables fintechs, non-custodial platforms, treasuries, and asset issuers to offer stablecoin yield products backed by real-world assets. It reports $200 million in total value locked against a stablecoin market that has now grown to more than $310 billion in supply.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-3">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>a16z Crypto's participation signals that RWA-backed stablecoin yield infrastructure is now considered a category with durable institutional demand, not a transitional product</li><li>OpenTrade's permissioned and permissionless dual architecture mirrors how institutional capital is approaching DeFi broadly: controlled access for compliance requirements alongside open rails for capital efficiency</li><li>At $310 billion in stablecoin supply, the quality and diversification of yield strategies backing stablecoin reserves becomes a material risk consideration for custodians and institutional issuers, not a secondary concern</li></ul><p>Source: <a href="https://www.coindesk.com/business/2026/05/06/opentrade-raises-usd17-million-to-expand-stablecoin-yield-infrastructure?ref=p2p.org" rel="noreferrer">CoinDesk, May 2026</a>.</p><h2 id="story-5-tokenized-private-credit-approaches-18-billion-as-institutional-defi-lending-matures">Story 5: Tokenized Private Credit Approaches $18 Billion as Institutional DeFi Lending Matures</h2><p>Tokenised private credit has grown to approximately $18 billion in active on-chain deployments, with Maple Finance leading the institutional segment with over $4 billion in assets under management. Analysts project tokenized private credit TVL to cross $40 billion by year-end 2026, based on current growth rates and the institutional product pipeline already announced for the second half of the year. Apollo Global Management's cooperation agreement with Morpho established the governance-heavy partnership template, with Ares and Carlyle identified as the most probable candidates for similar announcements by Q4 2026.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-4">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>As tokenized private credit approaches $40 billion, the blockchain networks settling these instruments face institutional scrutiny equivalent to that applied to traditional clearing and settlement infrastructure</li><li>The Apollo-Morpho template signals that traditional finance private credit managers are writing compliance specifications before deploying capital into DeFi protocols, raising the operational bar for validator infrastructure supporting these markets</li><li>Slashing events or validator downtime now carry credit market implications, not only network security implications, as staked assets increasingly serve as collateral in structured lending arrangements</li></ul><p>Source: <a href="https://financefeeds.com/tokenized-private-credit-in-2026-defis-18b-breakout-moment/?ref=p2p.org" rel="noreferrer">FinanceFeeds, May 2026</a>.</p><h2 id="key-takeaways-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams">Key Takeaways for Asset Managers, Custodians, Hedge Funds, ETF Issuers, Exchanges, and Staking Teams</h2><p>The first half of May 2026 surfaces five converging signals for institutional participants in on-chain infrastructure:</p><ul><li>The Federal Reserve has formally placed blockchain infrastructure reliability inside its financial stability assessment framework, signalling that supervisory expectations for validator and protocol operations are beginning to converge with those applied to traditional market infrastructure</li><li>Institutional stablecoin reserve architecture is moving onto proof-of-stake networks, with J.P. Morgan Asset Management and Anchorage Digital building the tokenized instrument layer that will sit inside reserve structures on Solana</li><li>Solana staking ETFs have crossed $1 billion in cumulative net inflows, with demand decoupling from price performance, confirming that institutional capital is structurally committed to proof-of-stake exposure through regulated product wrappers</li><li>RWA-backed stablecoin yield infrastructure is attracting tier-one venture capital and expanding to serve institutional treasury, custodian, and asset issuer use cases as the stablecoin market exceeds $310 billion in supply</li><li>Tokenized private credit is approaching $18 billion with a projected path to $40 billion by year-end, bringing traditional credit market governance expectations and validator reliability requirements into direct contact with DeFi lending protocol infrastructure</li></ul><p>👉 Subscribe to our newsletter at the bottom of this page to receive a monthly summary of the latest DeFi and staking developments, curated for institutional participants. Or follow us on <a href="https://linkedin.com/company/p2p-org?ref=p2p.org">LinkedIn</a> and <a href="https://twitter.com/p2pvalidator?ref=p2p.org">X</a> to stay updated when new DeFi Dispatch editions are published.</p><h2 id="frequently-asked-questions-faqs">Frequently Asked Questions (FAQs)<br></h2><h3 id="what-does-the-federal-reserves-commentary-on-tokenization-mean-for-institutional-staking-programs">What does the Federal Reserve's commentary on tokenization mean for institutional staking programs?</h3><p>When the Fed formally identifies blockchain infrastructure reliability as a financial stability consideration, it signals that validator uptime, slashing risk management, and protocol security are moving from technical due diligence items to supervisory expectations. Institutions building staking programs should expect these standards to be embedded in compliance and risk frameworks over the next 12 to 24 months.</p><h3 id="why-are-stablecoin-reserves-moving-onto-proof-of-stake-networks">Why are stablecoin reserves moving onto proof-of-stake networks?</h3><p>Static cash buffers generate no yield and create operational inefficiency at scale. Yield-bearing tokenized instruments held on proof-of-stake networks allow stablecoin issuers to earn protocol-native returns on reserve assets while maintaining on-demand liquidity through smart contract automation. As the stablecoin market exceeds $310 billion in supply, the capital efficiency advantage of this model over traditional reserve structures becomes material.</p><h3 id="what-is-tokenized-private-credit-and-why-does-it-matter-for-validator-infrastructure">What is tokenized private credit, and why does it matter for validator infrastructure?</h3><p>Tokenized private credit is on-chain lending backed by real-world business assets rather than crypto collateral. As this market scales toward $40 billion, staked assets are increasingly being used as collateral in structured lending arrangements, meaning validator downtime or slashing events carry credit market implications beyond network security. Institutions evaluating staking programs should factor credit market exposure into their validator selection and risk management frameworks.</p>

ALL

Agoric

Aptos

Auth

Avail

Avalanche

Axelar

Babylon

Bitcoin

bouldertech

BTC

capital flow

Cardano

Celestia

certifications

Chainlink

compliance

Cosmos

Crescent

curator

Cyberway

DAOBet

Data stream

DeFi

defi dispatch

defi infrastrcuture

defi infrastructure

defi news

defi vault

due diligence

DVT

Dymension

Economy

Education

EigenLayer

Elrond

employee

employee advocacy

employee interviews

ETF

Ethereum

Evmos

exit queue

Explain Like I'm Five

Governance

Guide

hedge fund

how to

HR

HUB series

Hyperliquid

infrastructure

institutional lens

institutional staking

Issuer

Kava

Kusama

landing

latin america

legal layer

legislation

Lido

liquid staking

LSP

Manta

Mantle

Marlin

Matic

MiCA

Moonbeam

MultiversX

Near

Networks

News

NuCypher

Oasis

Obol

Origin

P2P Verified

Partnership

pectra

Persistence

playbook

Pocket

Polkadot

Polygon

product

products

Quicksilver

Regen

regulation

Renzo

restaking

RPC Node

ALL

Agoric

Aptos

Auth

Avail

Avalanche

Axelar

Babylon

Bitcoin

bouldertech

BTC

capital flow

Cardano

Celestia

certifications

Chainlink

compliance

Cosmos

Crescent

curator

Cyberway

DAOBet

Data stream

DeFi

defi dispatch

defi infrastrcuture

defi infrastructure

defi news

defi vault

due diligence

DVT

Dymension

Economy

Education

EigenLayer

Elrond

employee

employee advocacy

employee interviews

ETF

Ethereum

Evmos

exit queue

Explain Like I'm Five

Governance

Guide

hedge fund

how to

HR

HUB series

Hyperliquid

infrastructure

institutional lens

institutional staking

Issuer

Kava

Kusama

landing

latin america

legal layer

legislation

Lido

liquid staking

LSP

Manta

Mantle

Marlin

Matic

MiCA

Moonbeam

MultiversX

Near

Networks

News

NuCypher

Oasis

Obol

Origin

P2P Verified

Partnership

pectra

Persistence

playbook

Pocket

Polkadot

Polygon

product

products

Quicksilver

Regen

regulation

Renzo

restaking

RPC Node