Travel Rule Enforcement and the Onchain Compliance Gap

Series: DeFi Infrastructure for Institutions

P2P.org's content series for regulated institutions evaluating on-chain capital allocation. Each article addresses a specific infrastructure, governance, or compliance dimension that determines whether a DeFi allocation can clear institutional approval and operate within mandate.

This is the second article in the regulatory trilogy examining the external pressure making institutional-grade vault governance a requirement rather than an option. The first article examined what MiCA means for DeFi vault operators and institutional allocators. The third article will examine how conflict-of-interest regulatory frameworks are catching up to the curator model.

Decentralised finance was built to remove intermediaries. The Travel Rule was built to hold intermediaries to account. That tension now sits at the centre of global AML supervision for anyone operating at the intersection of regulated institutions and DeFi vault infrastructure.

The Travel Rule is not a new concept. FATF Recommendation 16 has required originator and beneficiary information to accompany qualifying financial transfers since the 1990s, first for wire transfers, then extended to virtual assets in 2019. What is new is the enforcement environment. As of December 30, 2024, the EU's Transfer of Funds Regulation enforces the Travel Rule across all crypto-asset transfers involving a CASP with no minimum threshold. The UK has been enforcing its version since September 2023. As of early 2026, 73% of countries have enacted Travel Rule legislation. FATF updated Recommendation 16 again in June 2025 to further standardise cross-border payment information requirements. The era of aspirational Travel Rule compliance is over.

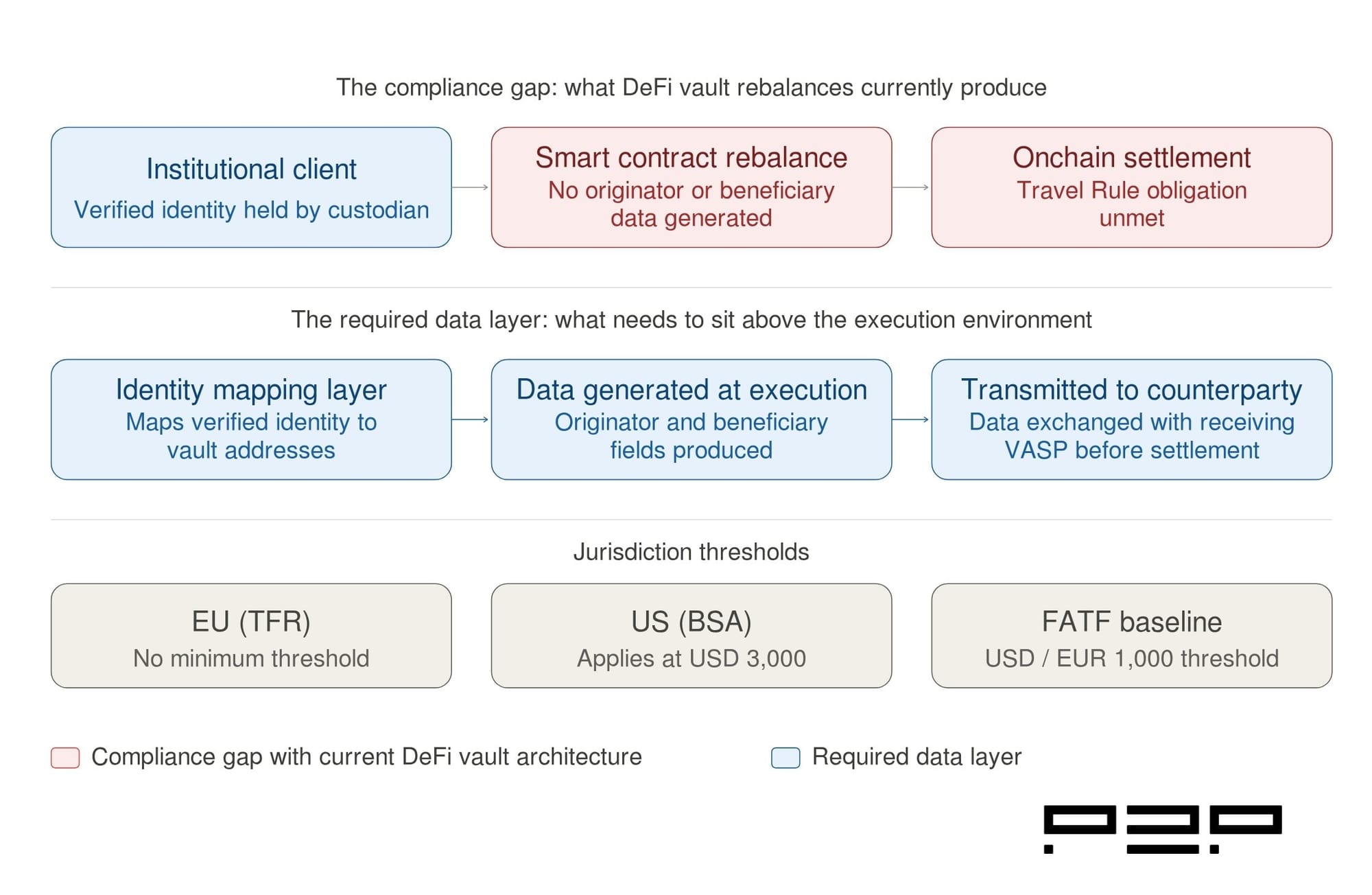

For DeFi vault operators and institutional allocators, the enforcement shift creates a specific and largely unresolved compliance problem. The Travel Rule requires a named originator and a named beneficiary to accompany every qualifying transfer. DeFi vault rebalances are executed by smart contracts. Smart contracts do not have names, addresses, or date-of-birth records. The data the Travel Rule requires does not exist in the architecture that executes the transaction.

This article explains what the Travel Rule requires mechanically, why DeFi vault architecture creates a structural compliance gap, how that gap affects both operators and institutional allocators in practice, and what the infrastructure requirement looks like for closing it.

The Travel Rule compliance gap in DeFi vault rebalances and the data layer required to close it.

Learnings for Busy Readers

Short on time? Here are the key takeaways. For the full analysis and supporting data, continue reading below.

The Travel Rule requires originator and beneficiary information, full name, account identifier, wallet address, and in higher-value transactions, physical address or date of birth, to accompany every qualifying crypto-asset transfer. In the EU, under the Transfer of Funds Regulation, this applies to every CASP-to-CASP transfer with no minimum threshold. In the US, the Bank Secrecy Act, it applies to transfers of $3,000 or more.

The compliance gap in DeFi vault architecture is architectural, not procedural. When a curator initiates a vault rebalance, the transaction is executed by a smart contract. The smart contract is not a VASP. It does not hold customer identity data. It cannot transmit originator and beneficiary information because that information does not exist in the execution layer. The entity that is a VASP, the custodian or service provider interacting with the vault on behalf of an institutional client, must generate that data from outside the protocol and attach it to the transaction before it settles.

Most vault products were not designed with this infrastructure in mind. The gap is not a minor operational adjustment. It requires a data architecture that sits above the smart contract execution layer, holds verified identity information for every institutional participant, maps that information to every vault transaction at the point of execution, and transmits it to counterparty VASPs in a format that satisfies jurisdiction-specific Travel Rule requirements.

For institutional allocators, the Travel Rule gap adds a due diligence requirement that sits entirely outside the protocol evaluation. Before initiating vault interactions through a custodian or service provider, institutions need to verify that their intermediary's Travel Rule infrastructure can generate compliant data for every vault transaction type, including rebalances initiated by smart contracts, not just for direct custody transfers.

What the Travel Rule Requires

The Travel Rule's core requirement is straightforward: when a VASP or CASP transmits virtual assets on behalf of a customer, it must collect and transmit specific identifying information about the originator and the beneficiary to the receiving institution. That information must travel with the transfer, not reside in a separate onboarding system.

The specific data requirements vary by jurisdiction. Under the EU Transfer of Funds Regulation, which applies from December 30, 2024, with no minimum threshold, every CASP-to-CASP transfer requires the originator's full name, account or wallet identifier, and either a physical address, official personal document number, customer identification number, or date of birth, plus the beneficiary's name and account identifier. Under the US Bank Secrecy Act, the threshold is $3,000, with requirements for the originator's full name, account or wallet number, physical address, and the amount and execution date of the transfer.

FATF's updated guidance, revised at the June 2025 Plenary, reinforces that the obligation applies wherever a financial service is being provided, regardless of whether the service is characterised as decentralised. The guidance is explicit that DeFi arrangements are not outside the scope if there are natural or legal persons who control or operate a service. As of the June 2025 FATF targeted update, 99 jurisdictions are advancing Travel Rule implementation. Only 21% of 138 assessed jurisdictions are fully compliant with FATF Recommendation 15, indicating that enforcement is still developing, but the direction is unambiguous. (Source: FATF Targeted Update, June 2025; Zyphe, VASP KYC Compliance, March 2026.)

The data must travel with the transfer in real time, not in a post-settlement report. This is the operationally demanding part. It requires infrastructure that can generate, verify, and transmit identity data at the point of transaction execution, not after the fact.

The Structural Compliance Gap in DeFi Vaults

The Travel Rule compliance gap in DeFi vault architecture is not a documentation problem. It is an architectural problem rooted in how vault transactions are initiated and executed.

In a standard vault rebalance, the curator identifies an allocation opportunity, proposes a strategy adjustment, and the vault smart contract executes the resulting transactions across one or more DeFi lending protocols. The smart contract is the execution agent. It is not a VASP. It does not hold customer identity data. It does not have a compliance function. It simply executes the instructions encoded in its logic and settles the resulting transactions on-chain.

This creates a specific Travel Rule problem with three dimensions.

The originator identification problem

The Travel Rule requires a named originator: the entity instructing the transfer, with verified identity data. In a vault rebalance, the instruction comes from the smart contract executing the curator's strategy. There is no named human originator in the execution layer. The custodian or service provider who originally deposited assets into the vault on behalf of the institutional client is the economic originator, but that relationship is not encoded in the transaction that the smart contract executes. Mapping the institutional client's identity data to the smart contract execution requires infrastructure that sits above the protocol layer and maintains that mapping at every transaction point.

The beneficiary identification problem

In a vault rebalance, assets move between protocol positions, not between named individuals or institutions. When a vault reallocates from one lending market to another, the beneficiary of the transaction is a smart contract address, not a person. Under the EU TFR, CASPs must assess whether a customer owns or controls a self-hosted wallet before making assets available for transfers over €1,000. A smart contract address is not a self-hosted wallet in the traditional sense. It is a protocol address. Generating compliant beneficiary data for smart contract destinations requires a classification and verification system that most vault products were not designed to include.

The interoperability problem

Even where a custodian has Travel Rule infrastructure for standard crypto transfers, that infrastructure may not be designed to handle the transaction types that DeFi vault rebalances generate. DeFi vault transactions can involve multiple protocols, multiple chains, wrapped assets, and liquidity pool interactions. Each of these transaction types raises specific questions about how the Travel Rule applies and how originator and beneficiary data should be structured. As of 2026, there is no universal standard for Travel Rule data transmission, though protocols like TRISA, OpenVASP, and TRUST are operating in parallel. A custodian whose Travel Rule infrastructure uses one protocol may be unable to exchange data with a counterparty using a different one.

The institutional digital asset space moves fast. Our subscribers get structured analysis across staking, DeFi vaults, and regulation through DeFi Dispatch, Institutional Lens, DeFi Infrastructure for Institutions, andLegal Layer. No noise. Just the signals that matter. Subscribe to the newsletter at the bottom of this page.

How the Gap Affects Vault Operators

For vault operators that fall within MiCA's CASP framework, or that serve clients in jurisdictions with equivalent Travel Rule obligations, the compliance gap is an operational infrastructure requirement that cannot be deferred.

The Travel Rule obligation attaches at the point where a CASP is involved in a transfer. A vault operator managing institutional assets is providing a service that places it within the CASP scope. Every vault transaction involving an institutional client's assets is a transaction that the vault operator's Travel Rule infrastructure must be able to process. That includes rebalances, protocol interactions, and position adjustments initiated by the vault's smart contract logic.

The practical requirement is a data layer that sits above the smart contract execution environment and performs three functions. First, it maintains a verified identity record for every institutional participant and maps that record to the vault addresses associated with their allocations. Second, it intercepts every transaction at the point of initiation, generates the required originator and beneficiary data from the identity record, and attaches that data to the transaction before it executes. Third, it transmits the data to counterparty VASPs in a format compatible with the applicable Travel Rule protocol and retains a timestamped record for regulatory audit purposes.

Under the EU TFR, originator and beneficiary data must be retained for five years after the end of the business relationship or transaction. That retention requirement is a data management obligation that extends well beyond the transaction itself. The vault operator's Travel Rule infrastructure must include a compliant data retention and retrieval system that can produce records on regulatory request.

How the Gap Affects Institutional Allocators

For institutional allocators, the Travel Rule gap creates a due diligence requirement that operates at the counterparty level rather than the protocol level.

The allocator's obligation is typically discharged through the custodian or service provider they use to interact with DeFi vault protocols. The custodian is the VASP. The custodian bears the Travel Rule obligation for transfers initiated on the allocator's behalf. But the allocator needs to verify, before initiating any vault interaction, that their custodian's Travel Rule infrastructure can handle the specific transaction types that vault interactions generate.

This verification requirement has three specific dimensions. First, the allocator needs to confirm that the custodian can generate compliant originator data for vault rebalances initiated by smart contracts, not just for direct custody transfers. The mapping of institutional identity to smart contract execution is the non-trivial part. Second, the allocator needs to confirm that the custodian can handle the vault's specific transaction types, including multi-protocol rebalances, wrapped asset interactions, and any cross-chain transactions the vault strategy involves. Third, the allocator needs to confirm that the custodian's Travel Rule protocol is interoperable with the counterparty VASPs involved in the vault's transaction flow.

For institutional allocators operating across multiple jurisdictions, the interoperability question is particularly complex. The EU applies the Travel Rule with no minimum threshold. The US applies it at $3,000. The UK applies a risk-based approach. Singapore, Hong Kong, and South Korea have their own implementations. A vault strategy that involves transactions across multiple jurisdictions requires Travel Rule infrastructure that can apply the correct data requirements for each transaction based on the jurisdictions of the parties involved.

The due diligence checklist for Travel Rule compliance is therefore not a protocol-level question. It is a custodian infrastructure question that needs to be resolved before vault interactions begin.

Key Takeaway

The Travel Rule's compliance gap in DeFi vault architecture is architectural. Smart contracts do not generate originator and beneficiary data. The vault products built on top of them were not designed to produce it. And the enforcement environment, with the EU TFR applying to every CASP transfer since December 30, 2024, and 73% of countries having enacted Travel Rule legislation as of early 2026, means the gap can no longer be treated as a future compliance consideration.

For vault operators, closing the gap requires a data layer above the smart contract execution environment that maps institutional identity to vault transactions, generates compliant Travel Rule data at the point of execution, and retains records in a format that satisfies the retention and retrieval requirements of the applicable jurisdictions.

For institutional allocators, it requires a custodian due diligence process that verifies Travel Rule infrastructure at the transaction-type level, not just at the general compliance framework level. The question is not whether the custodian is Travel Rule compliant. The question is whether the custodian's Travel Rule infrastructure can handle the specific transaction types that vault interactions generate.

The infrastructure that closes both gaps is the same infrastructure that the first trilogy of this series identified as the missing governance layer: an independent data and compliance layer sitting above the execution environment, operating at the transaction level, independently of the smart contracts executing the strategy.

Next in this series: How Conflict-of-Interest Regulatory Frameworks Are Catching Up to the Curator Model

Frequently Asked Questions

What is the Travel Rule, and why does it apply to DeFi vault operators?

The Travel Rule, based on FATF Recommendation 16, requires VASPs and CASPs to collect and transmit originator and beneficiary information alongside qualifying virtual asset transfers. It applies to vault operators because any entity providing crypto-asset portfolio management services to clients is providing a service that falls within the VASP or CASP scope under the applicable jurisdiction's definition. The obligation attaches at the service provider level, not the protocol level. The DeFi protocols the vault operator uses to execute transactions may not be regulated, but the vault operator managing institutional assets through those protocols is.

What data does the Travel Rule require to accompany a crypto-asset transfer?

Under the EU Transfer of Funds Regulation, which applies to all CASP-to-CASP transfers with no minimum threshold since December 30, 2024, the required data includes the originator's full name, account or wallet identifier, and either a physical address, official personal document number, customer identification number, or date of birth, plus the beneficiary's name and account identifier. Under the US Bank Secrecy Act, the threshold is $3,000, with requirements for the originator's full name, account or wallet number, and physical address. FATF's June 2025 update further standardised cross-border requirements, with national implementation timelines varying by jurisdiction.

Why is generating Travel Rule data for DeFi vault rebalances technically difficult?

Vault rebalances are executed by smart contracts, not by named human originators. The smart contract is not a VASP and does not hold customer identity data. Generating compliant Travel Rule data requires a separate data layer that maintains verified identity records for every institutional participant, maps those records to the vault addresses associated with their allocations, and intercepts every transaction at the point of initiation to attach the required originator and beneficiary data before the transaction executes. The beneficiary identification problem is equally challenging, as the beneficiary of a rebalance transaction is typically a protocol address rather than a named individual or institution.

What does Travel Rule interoperability mean, and why does it matter for vault operators?

Travel Rule interoperability refers to the ability of different VASPs' Travel Rule systems to exchange originator and beneficiary data with each other. Multiple competing protocols currently handle this data exchange, including TRISA, OpenVASP, and TRUST, and they are not universally compatible. A vault operator whose infrastructure uses one protocol may be unable to exchange data with a counterparty using a different one. For vault operators handling multi-protocol, multi-chain transactions, interoperability gaps can create compliance failures at specific transaction points even where the underlying data infrastructure is otherwise compliant.

What should institutional allocators verify about their custodian's Travel Rule infrastructure before initiating vault interactions?

Allocators should verify three things. First, the custodian can generate compliant originator data for vault rebalances initiated by smart contracts, not just for direct custody transfers. Second, the custodian's infrastructure can handle the specific transaction types involved in the vault strategy, including multi-protocol rebalances, wrapped asset interactions, and any cross-chain transactions. Third, the custodian's Travel Rule protocol is interoperable with the counterparty VASPs involved in the vault's transaction flow. These are infrastructure questions that need to be resolved before vault interactions begin, not after the first transaction fails a compliance check.

P2P.org builds the protection layer that sits between regulated institutions and DeFi execution environments, independently of the curators who manage allocation strategies. If you are evaluating the infrastructure requirements for a DeFi allocation program, talk to our team.

Disclaimer

This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or investment advice. Regulatory obligations may vary depending on jurisdiction and specific business activities. Readers should consult their own legal and compliance advisors regarding applicable requirements.

Subscribe to P2P-economy

Get the latest posts delivered right to your inbox

<hr><h2 id="series-defi-dispatch">Series: DeFi Dispatch</h2><p>DeFi Dispatch is <a href="http://p2p.org/?ref=p2p.org">P2P.org</a>'s twice-monthly roundup of DeFi developments for institutional participants. Each edition covers the signals that matter for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams operating at the intersection of traditional and on-chain finance.</p><p>👉 Subscribe to our newsletter at the bottom of this page to receive a monthly summary of the latest DeFi and staking developments, curated for institutional participants.</p><p>Missed the previous edition? Catch up here: <a href="https://p2p.org/economy/defi-dispatch-defi-news-april-2026-issue-2/">DeFi Dispatch: DeFi News and Signals April 2026 (Issue 2)</a></p><h2 id="quick-learnings-for-busy-readers">Quick Learnings for Busy Readers</h2><p>Short on time? Here are the key takeaways. For the full analysis, continue reading below.</p><p>The first half of May brought five developments that institutional participants in DeFi and staking infrastructure should track closely.</p><ul><li>A Federal Reserve Governor formally confirmed that U.S. tokenized assets have more than doubled to $25 billion, placing validator and protocol reliability inside the Fed's financial stability assessment framework for the first time.</li><li>Anchorage Digital and J.P. Morgan Asset Management announced a yield-bearing stablecoin reserve model on Solana, embedding proof-of-stake validator infrastructure directly into institutional stablecoin reserve management.</li><li>Solana staking ETFs crossed $1 billion in cumulative net inflows, with demand remaining positive even during periods of negative price performance, signalling institutional capital is allocating based on infrastructure conviction rather than short-term price momentum.</li><li>OpenTrade raised $17 million with participation from a16z Crypto to expand its stablecoin yield infrastructure backed by real-world assets, as the $310 billion stablecoin market drives structural demand for compliant, diversified yield strategies.</li><li>Tokenized private credit approached $18 billion in active on-chain deployment, with analysts projecting $40 billion by year-end as traditional finance private credit managers follow Apollo's governance-heavy DeFi protocol partnership model.</li></ul><h2 id="story-1-federal-reserve-governor-cook-confirms-us-tokenized-assets-have-doubled-to-25-billion">Story 1: Federal Reserve Governor Cook Confirms U.S. Tokenized Assets Have Doubled to $25 Billion</h2><p>Federal Reserve Governor Lisa Cook delivered a landmark speech on tokenization at the Central Bank of West African States Conference in Dakar on May 8, confirming that tokenized assets in the U.S. have more than doubled in market capitalization over the past year, reaching approximately $25 billion. Cook identified collateral and liquidity management as the primary institutional use case driving adoption, pointing to the intersection of large existing markets, including bonds, money market fund shares, and repurchase agreements, with opportunities for new functionality through automation and programmability.</p><p>Cook explicitly flagged smart contract and DeFi vulnerabilities as risks that could leave less room for human intervention when errors or attacks occur, placing validator and protocol reliability inside the Fed's systemic risk vocabulary for the first time. She also confirmed that the Federal Reserve is actively researching tokenization's implications and engaging with international organizations, peer central banks, and industry participants to monitor responsible innovation.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>A sitting Fed Governor formally framing blockchain infrastructure reliability as a financial stability consideration signals that supervisory expectations for validator and protocol operations are beginning to converge with those applied to traditional market infrastructure</li><li>Cook's identification of repo and collateral management as the primary tokenization use cases maps directly onto the on-chain settlement infrastructure already being built on Ethereum and Solana</li><li>For custodians and staking teams, the Fed's active engagement means operational standards for blockchain infrastructure are increasingly likely to be subject to formal supervisory expectations, not only market convention</li></ul><p>Source: <a href="https://finadium.com/feds-cook-says-collateral-and-liquidity-management-is-the-major-tokenization-use-case/?ref=p2p.org" rel="noreferrer">Federal Reserve Board, Finadium, May 2026</a>.</p><h2 id="story-2-anchorage-digital-and-jp-morgan-build-yield-bearing-stablecoin-reserves-on-solana">Story 2: Anchorage Digital and J.P. Morgan Build Yield-Bearing Stablecoin Reserves on Solana</h2><p>Anchorage Digital announced a cashless stablecoin reserve model on Solana on May 5, working with J.P. Morgan Asset Management to develop a tokenized instrument solution powering the liquidity framework. Rather than holding static cash buffers, the model holds reserves in yield-bearing, low-risk tokenized instruments on Solana that can generate on-demand liquidity, with Anchorage Digital issuing and managing stablecoins on behalf of institutional partners under this structure.</p><p>Anchorage Digital already serves as the regulated custodian for Tether's U.S. stablecoin, Ethena's stablecoin, Western Union's stablecoin, and BlackRock's BUIDL. Every architecture decision it makes about where reserve assets are held carries ecosystem-wide implications for which blockchain networks attract institutional reserve capital.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-1">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>Yield-bearing stablecoin reserves on a proof-of-stake network require that network to operate with institutional-grade uptime and performance, making Solana validator infrastructure part of the reserve management stack</li><li>J.P. Morgan Asset Management's involvement signals that the largest traditional asset managers are now actively designing the tokenized instrument layer that will sit inside stablecoin reserve structures</li><li>For staking product managers and validator operators, this announcement represents the clearest signal yet that institutional stablecoin infrastructure and proof-of-stake network participation are converging into a single operational layer</li></ul><p>Source: <a href="https://www.pymnts.com/cryptocurrency/2026/anchorage-digital-pursues-more-efficient-institutional-stablecoin-liquidity/?ref=p2p.org" rel="noreferrer">Anchorage Digital, PYMNTS, May 2026</a>.</p><h2 id="story-3-solana-staking-etfs-cross-1-billion-in-cumulative-net-inflows">Story 3: Solana Staking ETFs Cross $1 Billion in Cumulative Net Inflows</h2><p>SOL spot ETFs recorded a net inflow of $21.3 million on May 6, with the Bitwise Solana Staking ETF leading at $20.77 million in single-day inflows and bringing its total assets to $850 million. Historical cumulative net inflows across all SOL spot ETFs crossed $1.044 billion, with Bitwise alone recording $8.5 billion in cumulative historical net inflows since launch.</p><p>Solana staking ETF inflows have remained positive despite negative price performance for SOL over several months, a pattern that decouples from conventional risk-on and risk-off behaviour in crypto markets. The Fidelity Solana Fund ETF fee waiver expires May 18, after which a 0.25% expense ratio and 15% staking fee apply, making this an important test of whether institutional demand sustains once full fee loads are introduced.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-2">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>Inflows remaining positive through price drawdowns signal institutional capital is allocating based on infrastructure conviction rather than short-term price momentum, a more durable demand driver for validator infrastructure</li><li>The fee competition among Bitwise, Fidelity, and Grayscale establishes the economic reference points that will govern how validator infrastructure is priced within regulated product wrappers</li><li>Crossing $1 billion in cumulative inflows confirms that staking-enabled ETF products have found sustained institutional demand beyond the launch window</li></ul><p>Source: <a href="https://coin360.com/news/fidelity-solana-staking-etf-launch-institutional-shift?ref=p2p.org" rel="noreferrer">SoSoValue via KuCoin, Coin360, Solana Compass, May 2026</a>.</p><h2 id="story-4-opentrade-raises-17-million-to-expand-stablecoin-yield-infrastructure-backed-by-real-world-assets">Story 4: OpenTrade Raises $17 Million to Expand Stablecoin Yield Infrastructure Backed by Real-World Assets</h2><p>Stablecoin infrastructure platform OpenTrade raised $17 million on May 6 in a round led by Mercury Fund and Notion Capital, with participation from a16z Crypto, bringing its total funding to more than $30 million. The firm enables fintechs, non-custodial platforms, treasuries, and asset issuers to offer stablecoin yield products backed by real-world assets. It reports $200 million in total value locked against a stablecoin market that has now grown to more than $310 billion in supply.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-3">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>a16z Crypto's participation signals that RWA-backed stablecoin yield infrastructure is now considered a category with durable institutional demand, not a transitional product</li><li>OpenTrade's permissioned and permissionless dual architecture mirrors how institutional capital is approaching DeFi broadly: controlled access for compliance requirements alongside open rails for capital efficiency</li><li>At $310 billion in stablecoin supply, the quality and diversification of yield strategies backing stablecoin reserves becomes a material risk consideration for custodians and institutional issuers, not a secondary concern</li></ul><p>Source: <a href="https://www.coindesk.com/business/2026/05/06/opentrade-raises-usd17-million-to-expand-stablecoin-yield-infrastructure?ref=p2p.org" rel="noreferrer">CoinDesk, May 2026</a>.</p><h2 id="story-5-tokenized-private-credit-approaches-18-billion-as-institutional-defi-lending-matures">Story 5: Tokenized Private Credit Approaches $18 Billion as Institutional DeFi Lending Matures</h2><p>Tokenised private credit has grown to approximately $18 billion in active on-chain deployments, with Maple Finance leading the institutional segment with over $4 billion in assets under management. Analysts project tokenized private credit TVL to cross $40 billion by year-end 2026, based on current growth rates and the institutional product pipeline already announced for the second half of the year. Apollo Global Management's cooperation agreement with Morpho established the governance-heavy partnership template, with Ares and Carlyle identified as the most probable candidates for similar announcements by Q4 2026.</p><h3 id="why-is-this-important-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams-4">Why is this important for asset managers, custodians, hedge funds, ETF issuers, exchanges, and staking teams?</h3><ul><li>As tokenized private credit approaches $40 billion, the blockchain networks settling these instruments face institutional scrutiny equivalent to that applied to traditional clearing and settlement infrastructure</li><li>The Apollo-Morpho template signals that traditional finance private credit managers are writing compliance specifications before deploying capital into DeFi protocols, raising the operational bar for validator infrastructure supporting these markets</li><li>Slashing events or validator downtime now carry credit market implications, not only network security implications, as staked assets increasingly serve as collateral in structured lending arrangements</li></ul><p>Source: <a href="https://financefeeds.com/tokenized-private-credit-in-2026-defis-18b-breakout-moment/?ref=p2p.org" rel="noreferrer">FinanceFeeds, May 2026</a>.</p><h2 id="key-takeaways-for-asset-managers-custodians-hedge-funds-etf-issuers-exchanges-and-staking-teams">Key Takeaways for Asset Managers, Custodians, Hedge Funds, ETF Issuers, Exchanges, and Staking Teams</h2><p>The first half of May 2026 surfaces five converging signals for institutional participants in on-chain infrastructure:</p><ul><li>The Federal Reserve has formally placed blockchain infrastructure reliability inside its financial stability assessment framework, signalling that supervisory expectations for validator and protocol operations are beginning to converge with those applied to traditional market infrastructure</li><li>Institutional stablecoin reserve architecture is moving onto proof-of-stake networks, with J.P. Morgan Asset Management and Anchorage Digital building the tokenized instrument layer that will sit inside reserve structures on Solana</li><li>Solana staking ETFs have crossed $1 billion in cumulative net inflows, with demand decoupling from price performance, confirming that institutional capital is structurally committed to proof-of-stake exposure through regulated product wrappers</li><li>RWA-backed stablecoin yield infrastructure is attracting tier-one venture capital and expanding to serve institutional treasury, custodian, and asset issuer use cases as the stablecoin market exceeds $310 billion in supply</li><li>Tokenized private credit is approaching $18 billion with a projected path to $40 billion by year-end, bringing traditional credit market governance expectations and validator reliability requirements into direct contact with DeFi lending protocol infrastructure</li></ul><p>👉 Subscribe to our newsletter at the bottom of this page to receive a monthly summary of the latest DeFi and staking developments, curated for institutional participants. Or follow us on <a href="https://linkedin.com/company/p2p-org?ref=p2p.org">LinkedIn</a> and <a href="https://twitter.com/p2pvalidator?ref=p2p.org">X</a> to stay updated when new DeFi Dispatch editions are published.</p><h2 id="frequently-asked-questions-faqs">Frequently Asked Questions (FAQs)<br></h2><h3 id="what-does-the-federal-reserves-commentary-on-tokenization-mean-for-institutional-staking-programs">What does the Federal Reserve's commentary on tokenization mean for institutional staking programs?</h3><p>When the Fed formally identifies blockchain infrastructure reliability as a financial stability consideration, it signals that validator uptime, slashing risk management, and protocol security are moving from technical due diligence items to supervisory expectations. Institutions building staking programs should expect these standards to be embedded in compliance and risk frameworks over the next 12 to 24 months.</p><h3 id="why-are-stablecoin-reserves-moving-onto-proof-of-stake-networks">Why are stablecoin reserves moving onto proof-of-stake networks?</h3><p>Static cash buffers generate no yield and create operational inefficiency at scale. Yield-bearing tokenized instruments held on proof-of-stake networks allow stablecoin issuers to earn protocol-native returns on reserve assets while maintaining on-demand liquidity through smart contract automation. As the stablecoin market exceeds $310 billion in supply, the capital efficiency advantage of this model over traditional reserve structures becomes material.</p><h3 id="what-is-tokenized-private-credit-and-why-does-it-matter-for-validator-infrastructure">What is tokenized private credit, and why does it matter for validator infrastructure?</h3><p>Tokenized private credit is on-chain lending backed by real-world business assets rather than crypto collateral. As this market scales toward $40 billion, staked assets are increasingly being used as collateral in structured lending arrangements, meaning validator downtime or slashing events carry credit market implications beyond network security. Institutions evaluating staking programs should factor credit market exposure into their validator selection and risk management frameworks.</p>

<p><strong>Series:</strong> Institutional Lens | Validation Infrastructure</p><p>The Institutional Lens series unpacks the protocol mechanics, infrastructure decisions, and governance considerations that matter most for institutional participants in proof-of-stake networks. Each article is written for professionals operating at the intersection of traditional finance and blockchain infrastructure, including digital asset custodians, crypto-native funds, ETF issuers, treasury teams, and staking product managers.</p><p><strong>Previously in the series:</strong> <a href="https://p2p.org/economy/why-institutional-capital-needs-a-protection-layer-in-proof-of-stake-networks/">Why Institutional Capital Needs a Protection Layer in Proof-of-Stake Networks</a></p><h2 id="introduction">Introduction</h2><p>Solana has crossed a threshold that changes how institutional participants need to think about it. Total Payment Volume on Solana surged 755% year-over-year, driven by institutional adoption and approximately $950 million in ETF inflows (Source: <a href="https://www.ainvest.com/news/sol-sees-strong-staking-transaction-growth-institutional-interest-2026-2603/?ref=p2p.org">Ainvest</a>). The March 2026 SEC and CFTC joint interpretation explicitly classified SOL as a digital commodity and confirmed that solo, self-custodial, custodial, and liquid staking models do not constitute securities transactions. The regulatory overhang that kept many compliance teams on the sidelines is gone.</p><p>What remains is a decision that carries more institutional weight than most teams have yet appreciated. The question is not whether to stake SOL, but how. For digital asset custodians, crypto-native funds, ETF issuers, treasury teams, and staking product managers, Solana staking for institutions is not a single product. Native staking and liquid staking are structurally different risk profiles, custody architectures, and capital management frameworks. Getting this decision right is as important as the allocation decision itself.</p><h2 id="learnings-for-busy-readers"><strong>Learnings for Busy Readers</strong></h2><p>What this article covers:</p><ul><li>How native and liquid staking differ structurally, not just mechanically</li><li>The risk, custody, and liquidity implications of each for institutional participants</li><li>How the current market shift across ETF approvals, LST fragmentation, and Alpenglow changes the calculus</li><li>A decision framework and due diligence checklist for institutional teams</li></ul><p><strong>The core argument:</strong> Native staking offers full custody control, no smart contract exposure, and a clean compliance posture. Liquid staking offers capital efficiency and DeFi composability at the cost of additional risk layers. For most institutional mandates, the right answer is not one or the other. It is understanding exactly which tradeoffs your organisation is equipped to underwrite.</p><h2 id="the-decision-is-not-what-most-teams-think-it-is">The Decision Is Not What Most Teams Think It Is</h2><p>The most common framing of the native vs. liquid staking question in Solana staking for institutions is a yield question. Native staking currently generates 5 to 7% APY depending on validator performance and commission rates, while liquid staking tokens such as JitoSOL and JupSOL generate between 5.89% and 6.16% APY as of early 2026, with some protocols reaching higher during periods of elevated network activity (Source: <a href="https://sanctum.so/blog/best-solana-yield-2026-staking-vs-defi?ref=p2p.org">Sanctum</a>).</p><p>For retail participants, the yield differential is the dominant consideration. For institutional participants, it is rarely the right place to start. The correct framing is a risk architecture question: what risk layers is your organisation prepared to accept, and does your mandate permit them?</p><p>Native staking and liquid staking expose participants to materially different risk categories. Understanding those categories, not the APY differential, is the foundation of a defensible institutional staking framework on Solana.</p><h2 id="native-staking-the-institutional-baseline">Native Staking: The Institutional Baseline</h2><p>In native staking, SOL is delegated directly from a client-controlled wallet to a validator. The delegator retains full custody of the private keys. The staked SOL never leaves the delegator's control. It is locked for voting weight purposes, not transferred to a third party.</p><p><strong>What native staking provides for institutions:</strong></p><p><strong>Full non-custodial architecture.</strong> The validator never holds client assets. Delegation is an instruction, not a transfer. This is structurally aligned with the non-custodial infrastructure model that institutional compliance frameworks typically require.</p><p><strong>No smart contract risk.</strong> Native staking operates at the protocol layer. There is no additional smart contract between the delegator and the network. The only code risk is Solana's base layer itself.</p><p><strong>Clean regulatory posture.</strong> The March 2026 SEC and CFTC interpretation explicitly confirmed that self-custodial staking with a third-party validator, where the custodian acts as agent and does not determine staking amounts or fix reward rates, is not a securities transaction. Native staking maps directly to this definition.</p><p><strong>Predictable reward mechanics.</strong> Protocol-generated rewards accrue each epoch, approximately every two days, are denominated in SOL, and compound automatically into the staked balance. Reward rates are determined entirely by network conditions.</p><p><strong>The institutional tradeoff:</strong></p><p>The primary constraint of native staking for institutions is liquidity. Native staking locks SOL for approximately two epochs, around four to five days, when unstaking is initiated (Source: <a href="https://hittincorners.com/guides/solana-liquid-staking-complete-guide-2026/?ref=p2p.org">HittinCorners</a>). For treasury teams managing redemption obligations or funds with liquidity covenants, this is a material consideration. It is not a disqualifying one, but it needs to be accounted for in position sizing and liquidity management frameworks before capital is deployed.</p><p>The secondary consideration is validator selection. In native staking, the delegator chooses a specific validator. That choice has direct implications for reward performance, slashing risk exposure, and governance representation. It is an active decision that requires due diligence, not a passive one.</p><h2 id="liquid-staking-capital-efficiency-with-additional-risk-layers">Liquid Staking: Capital Efficiency with Additional Risk Layers</h2><p>In liquid staking, SOL is deposited into a staking protocol such as Jito, Marinade, or Sanctum, which delegates to a set of validators and issues a liquid staking token (LST) representing the staked position plus accrued rewards. The LST can be traded, used as collateral in DeFi protocols, or swapped back to SOL through liquidity pools.</p><p>Over $3.3 billion in SOL is liquid-staked across Jito, DoubleZero, Marinade, and Sanctum as of early 2026, representing approximately 10 to 15% of all staked SOL. The segment is growing rapidly and is increasingly the focus of institutional product development.</p><p><strong>What liquid staking adds for institutions:</strong></p><p><strong>Liquidity.</strong> LSTs can be swapped back to SOL near-instantly through liquidity pools, removing the epoch lock-up constraint of native staking.</p><p><strong>DeFi composability.</strong> LSTs can be used as collateral on lending protocols, provided as liquidity in AMM pools, or deployed in structured yield strategies. This unlocks additional reward layers on top of the base staking rate, a meaningful consideration for institutions seeking to maximise capital efficiency.</p><p><strong>MEV distribution.</strong> Protocols like Jito pass a portion of MEV block tips to LST holders, which is why JitoSOL consistently generates a modest premium above the base native staking rate.</p><p><strong>The institutional risk calculus:</strong></p><p>Liquid staking for institutions introduces risk categories that native staking does not. Every institutional team evaluating LSTs needs to assess these explicitly.</p><p><strong>Smart contract risk.</strong> The LST protocol itself is a smart contract. Vulnerabilities in that contract represent a risk to staked capital that does not exist in native staking. The relevant question is not whether a protocol has been audited, as most have been, but whether your mandate permits smart contract exposure at all, and whether the protocol's audit history and incident record are acceptable to your risk committee.</p><p><strong>LST depeg risk.</strong> Under market stress, LSTs can trade below their underlying SOL value. During periods of stress, LSTs can trade below their underlying asset value. Institutions should maintain sufficient liquidity buffers and avoid over-leveraging LST positions (<a href="https://www.cobo.com/post/liquid-staking-for-institutions-complete-mpc-infrastructure-guide?ref=p2p.org">Cobo</a>). For funds with mark-to-market accounting obligations, a temporary depeg is a profit and loss event regardless of whether the underlying position eventually recovers.</p><p><strong>Validator concentration risk.</strong> LST protocols delegate to validator sets according to their own algorithms. The delegator has no direct control over validator selection. This matters for institutions with specific governance obligations, as they are effectively delegating governance representation to the protocol's delegation strategy rather than making that decision directly.</p><p><strong>Custody and compliance complexity.</strong> LSTs are tokens, not staking positions. Their treatment for accounting, tax reporting, and regulatory classification may differ from native staked SOL depending on jurisdiction. This is an active area of legal development and warrants specific advice for each institution.</p><h2 id="what-is-changing-right-now-and-why-it-matters">What Is Changing Right Now and Why It Matters</h2><p>Three developments in early 2026 have materially shifted the landscape for Solana staking for institutions.</p><p><strong>The SEC and CFTC commodity ruling.</strong> The March 17 joint interpretation formally cleared all four staking models, including liquid staking, as non-securities activities. For compliance teams that had blocked LST exposure pending regulatory clarity, that barrier is now removed. The question shifts from whether an institution can participate to whether it should, and under what framework.</p><p><strong>LST market fragmentation.</strong> JitoSOL's dominance is fracturing. Nasdaq filed a proposal in February 2026 to list the VanEck JitoSOL Solana Liquid Staking ETF, the first attempt to offer a regulated product tied directly to an LST. Galaxy Digital launched institutional SOL staking in March 2026. Hex Trust integrated JitoSOL for custodial staking, signalling that traditional custodians are beginning to treat LSTs as standard yield products. The LST landscape is maturing rapidly, but it is also becoming more complex. Institutions entering now face more protocol choices, more counterparty relationships, and more due diligence surface area than existed twelve months ago.</p><p><strong>Alpenglow's impact on native staking economics.</strong> The Alpenglow upgrade, approved by 98% of validators and deploying in 2026, will eliminate validator voting fees entirely. The elimination of voting fees means validators keep a larger portion of their earnings, effectively making staking more profitable for both validators and delegators, particularly for smaller operators who were previously losing a higher percentage of rewards to mandatory voting costs (Source: <a href="https://phemex.com/blogs/solana-alpenglow-upgrade-finality-explained?ref=p2p.org">Phemex</a>). For institutions in native staking programs, this represents an improvement in net reward rates without any change to risk posture, a meaningful compression of the native vs. liquid yield differential.</p><h2 id="the-institutional-decision-framework">The Institutional Decision Framework</h2><p>This is not a binary choice. Many institutional programs will run both: native staking for their core, compliance-sensitive position, and a controlled LST allocation where the mandate permits and the risk framework supports it. The relevant questions for each component are the following.</p><p><strong>For native Solana staking for institutions:</strong></p><p>Is your custody architecture non-custodial and client-controlled? Have you conducted due diligence on your validator's infrastructure, incident history, and governance posture? Is your liquidity management framework designed around the epoch lock-up timeline? Does your reward reporting infrastructure support validator-level attribution for accounting and audit purposes?</p><p><strong>For liquid staking as an institutional layer:</strong></p><p>Does your mandate permit smart contract exposure, and has legal confirmed the applicable standard? Has your risk committee reviewed the specific protocol's audit history, slashing incident record, and depeg history? Does your accounting framework have a defined treatment for LST mark-to-market movements? Are you clear on the tax treatment of LST rewards in each operating jurisdiction? Is the validator governance delegation of the LST protocol acceptable, given that the protocol determines it rather than you?</p><p><a href="http://p2p.org/?ref=p2p.org">P2P.org</a>'s <a href="https://p2p.org/networks/solana?ref=p2p.org">Solana staking infrastructure</a> is built for institutional native staking with non-custodial architecture, validator-level reporting, geographically distributed infrastructure, and operational safeguards aligned with the risk posture institutional partners require. Our <a href="https://docs.p2p.org/?ref=p2p.org">technical documentation</a> provides detailed guidance on integration, reward reporting, and operational architecture for teams building or evaluating a Solana staking program.</p><figure class="kg-card kg-image-card"><img src="https://p2p.org/economy/content/images/2026/05/Native-vs.-liquid-staking-on-Solana-compared-across-custody--smart-contract-risk--liquidity--and-governance-dimensions-for-institutional-allocators..png" class="kg-image" alt="Native vs. liquid staking on Solana compared across custody, smart contract risk, liquidity, and governance dimensions for institutional allocators." loading="lazy" width="1600" height="900" srcset="https://p2p.org/economy/content/images/size/w600/2026/05/Native-vs.-liquid-staking-on-Solana-compared-across-custody--smart-contract-risk--liquidity--and-governance-dimensions-for-institutional-allocators..png 600w, https://p2p.org/economy/content/images/size/w1000/2026/05/Native-vs.-liquid-staking-on-Solana-compared-across-custody--smart-contract-risk--liquidity--and-governance-dimensions-for-institutional-allocators..png 1000w, https://p2p.org/economy/content/images/2026/05/Native-vs.-liquid-staking-on-Solana-compared-across-custody--smart-contract-risk--liquidity--and-governance-dimensions-for-institutional-allocators..png 1600w" sizes="(min-width: 720px) 720px"></figure><p><strong>Ready to build your Solana staking program on institutional-grade infrastructure?</strong> <a href="http://p2p.org/?ref=p2p.org">P2P.org</a> provides non-custodial, validator-level Solana staking for institutions with full reward attribution and reporting built in. <a href="https://p2p.org/networks/solana?ref=p2p.org">Explore P2P.org Solana Staking</a></p><h2 id="due-diligence-checklist">Due Diligence Checklist</h2><p>For staking product managers, risk committees, and compliance teams evaluating a Solana staking structure.</p><p><strong>Native staking:</strong></p><ul><li>[ ] Custody architecture is non-custodial with client keys and client control</li><li>[ ] Validator selected based on infrastructure quality, incident history, and geographic distribution</li><li>[ ] Epoch lock-up timeline integrated into liquidity management framework</li><li>[ ] Validator-level reward reporting available in accounting-compatible format</li><li>[ ] Validator governance participation policy documented</li><li>[ ] SLA framed around operational practices, not performance guarantees</li></ul><p><strong>Liquid staking (additional layer):</strong></p><ul><li>[ ] Smart contract audit history reviewed and accepted by the risk committee</li><li>[ ] Slashing incident and depeg history reviewed for selected protocol</li><li>[ ] LST accounting treatment confirmed with legal and finance teams</li><li>[ ] Tax treatment of LST rewards confirmed per operating jurisdiction</li><li>[ ] The validator delegation strategy of the protocol is reviewed and acceptable</li><li>[ ] DeFi deployment strategy, if any, has independent risk approval</li></ul><h2 id="key-takeaway">Key Takeaway</h2><p>For institutional participants in Solana's proof-of-stake network, the native vs. liquid staking decision is not primarily about yield optimisation. It is about risk architecture, custody posture, and mandate alignment. Native staking provides the cleanest institutional baseline with full custody control, no smart contract exposure, and a regulatory posture that maps directly to the March 2026 SEC and CFTC interpretation. Liquid staking offers capital efficiency and composability at the cost of additional risk layers that each institution must explicitly evaluate and accept.</p><p>With Alpenglow improving native staking economics, the SEC commodity ruling removing regulatory ambiguity, and the LST market becoming more complex rather than simpler, the case for starting with a rigorous native staking foundation has never been stronger. Build the baseline correctly, then evaluate whether your mandate and risk framework support expanding from there.</p><p><em>Protocol-generated rewards are determined by network conditions and are variable. </em><a href="http://p2p.org/?ref=p2p.org"><em>P2P.org</em></a><em> does not control or set reward rates. Slashing risks are protocol-defined and client-borne. Operational safeguards are implemented to reduce slashing exposure, but do not eliminate protocol-level risk.</em></p><h2 id="faq">FAQ</h2><p><strong>What is the difference between native staking and liquid staking for Solana institutional programs?</strong></p><p>In native staking, SOL is delegated directly from a client-controlled wallet to a validator. The delegator retains full custody at all times, and the staked SOL never leaves their control. In liquid staking, SOL is deposited into a protocol which issues a liquid staking token representing the staked position. The LST can be traded or used in DeFi, but introduces additional risk layers, including smart contract exposure and potential depeg risk that native staking does not carry.</p><p><strong>Is liquid staking on Solana permitted under institutional mandates following the March 2026 ruling?</strong></p><p>As of March 17, 2026, the SEC and CFTC jointly confirmed that liquid staking activities do not constitute securities transactions, provided the provider does not fix or guarantee reward amounts. This ruling removed the primary regulatory barrier that had previously caused many institutional compliance teams to restrict LST exposure. Whether a specific mandate permits LST exposure remains a question for each institution's legal and risk teams.</p><p><strong>How does the Alpenglow upgrade affect Solana staking for institutions?</strong></p><p>Alpenglow eliminates validator voting fees, which had previously represented a meaningful operating cost, reducing net rewards for both validators and delegators. When deployed in 2026, it improves the net reward rate of native staking programs without changing their risk posture. This compresses the yield differential between native and liquid staking, making native staking more competitive for institutions where the additional risk layers of LSTs are not warranted by the mandate.</p><p><strong>What is the unstaking timeline for institutional native SOL staking?</strong></p><p>Native SOL staking has an unstaking period of approximately two epochs, or around four to five days under normal network conditions. This lock-up period is a material liquidity consideration for institutional programs and should be integrated into position sizing and liquidity management frameworks before capital is deployed.</p><p><strong>How should institutions account for liquid staking tokens?</strong></p><p>LSTs are tokens representing staked positions and accrued rewards. Their accounting treatment, particularly for mark-to-market movements, reward recognition, and tax treatment, may differ from native staked SOL depending on jurisdiction and applicable accounting standards. Institutions should obtain specific legal and accounting guidance for their operating jurisdiction before deploying into LST positions.</p><p><strong>What due diligence should institutions conduct on a liquid staking protocol?</strong></p><p>Key areas include the protocol's smart contract audit history and any prior incidents, its slashing and depeg history, its validator delegation strategy and whether it aligns with governance obligations, the accounting and tax treatment of LST rewards in the relevant jurisdiction, and whether the protocol has had independent security reviews by recognised firms.</p><hr><p><strong><em>Disclaimer</em></strong></p><p>This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or investment advice. Regulatory obligations may vary depending on jurisdiction and specific business activities. Readers should consult their own legal and compliance advisors regarding applicable requirements.</p>

ALL

Agoric

Aptos

Auth

Avail

Avalanche

Axelar

Babylon

Bitcoin

bouldertech

BTC

capital flow

Cardano

Celestia

certifications

Chainlink

compliance

Cosmos

Crescent

curator

Cyberway

DAOBet

Data stream

DeFi

defi dispatch

defi infrastrcuture

defi infrastructure

defi news

defi vault

due diligence

DVT

Dymension

Economy

Education

EigenLayer

Elrond

employee

employee advocacy

employee interviews

ETF

Ethereum

Evmos

exit queue

Explain Like I'm Five

Governance

Guide

hedge fund

how to

HR

HUB series

Hyperliquid

infrastructure

institutional lens

institutional staking

Issuer

Kava

Kusama

landing

latin america

legal layer

legislation

Lido

liquid staking

LSP

Manta

Mantle

Marlin

Matic

MiCA

Moonbeam

MultiversX

Near

Networks

News

NuCypher

Oasis

Obol

Origin

P2P Verified

Partnership

pectra

Persistence

playbook

Pocket

Polkadot

Polygon

product

products

Quicksilver

Regen

regulation

Renzo

restaking

RPC Node

ALL

Agoric

Aptos

Auth

Avail

Avalanche

Axelar

Babylon

Bitcoin

bouldertech

BTC

capital flow

Cardano

Celestia

certifications

Chainlink

compliance

Cosmos

Crescent

curator

Cyberway

DAOBet

Data stream

DeFi

defi dispatch

defi infrastrcuture

defi infrastructure

defi news

defi vault

due diligence

DVT

Dymension

Economy

Education

EigenLayer

Elrond

employee

employee advocacy

employee interviews

ETF

Ethereum

Evmos

exit queue

Explain Like I'm Five

Governance

Guide

hedge fund

how to

HR

HUB series

Hyperliquid

infrastructure

institutional lens

institutional staking

Issuer

Kava

Kusama

landing

latin america

legal layer

legislation

Lido

liquid staking

LSP

Manta

Mantle

Marlin

Matic

MiCA

Moonbeam

MultiversX

Near

Networks

News

NuCypher

Oasis

Obol

Origin

P2P Verified

Partnership

pectra

Persistence

playbook

Pocket

Polkadot

Polygon

product

products

Quicksilver

Regen

regulation

Renzo

restaking

RPC Node