What MiCA Means for DeFi Vault Operators and Institutional Allocators

Series: DeFi Infrastructure for Institutions

P2P.org's content series for regulated institutions evaluating on-chain capital allocation. Each article addresses a specific infrastructure, governance, or compliance dimension that determines whether a DeFi allocation can clear institutional approval and operate within mandate.

This article opens the second trilogy in the series, examining the regulatory environment that is accelerating the infrastructure requirement for institutional DeFi allocation. The first trilogy established the structural gap: why DeFi vault architecture was not built for institutional risk tolerance, why the curator incentive structure creates a conflict of interest, and why mandate validation at execution is the governance standard institutions require. This trilogy examines the external pressure making that governance standard a regulatory inevitability rather than an optional upgrade.

MiCA came into force on December 30, 2024. Its stablecoin provisions had already been applied since June 2024. The Transfer of Funds Regulation, which enforces the Travel Rule across crypto-asset transfers, became enforceable the same day. Seven countries outside the EU are actively drafting MiCA-style regulations. The era of regulatory arbitrage within Europe is over.

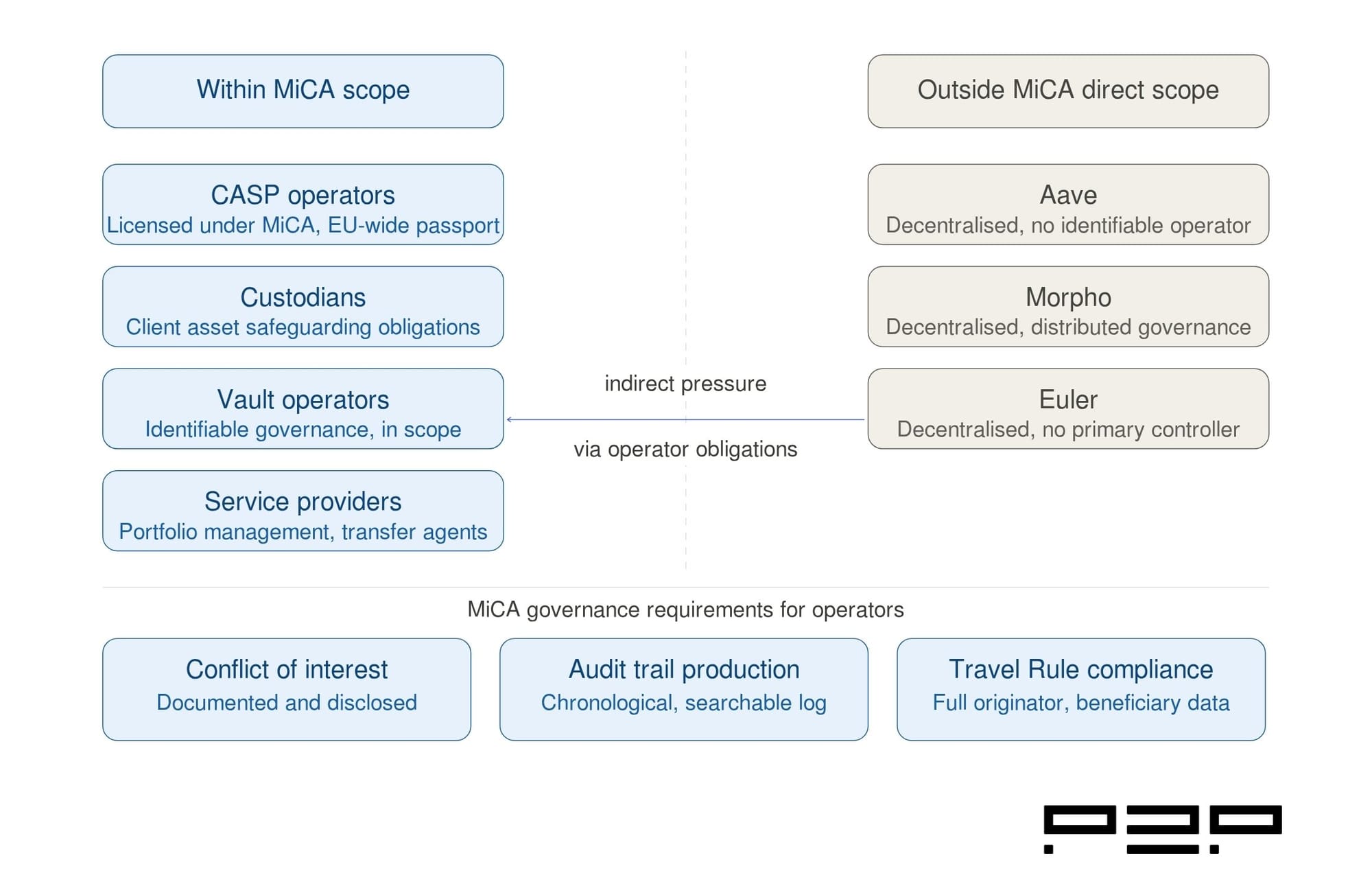

And yet MiCA explicitly excludes fully decentralised DeFi protocols from its scope. Protocols like Aave, Morpho, and Euler, where no identifiable entity manages the primary functions, are not directly regulated by MiCA. The regulation is designed for centralised entities: issuers, exchanges, custodians, and service providers.

This creates an apparent paradox that institutional allocators and vault operators evaluating DeFi exposure need to understand clearly. MiCA does not regulate the protocols. But it comprehensively regulates the entities that interact with them on behalf of institutional clients. And it introduces governance requirements around conflict of interest management, audit trail production, and role separation that map directly onto the three structural gaps the first trilogy of this series identified.

The result is not that MiCA makes DeFi allocation impossible. It is that MiCA makes the governance infrastructure required to do DeFi allocation compliant non-negotiable for any regulated entity operating within its scope.

What MiCA regulates directly, what falls outside its scope, and the three governance requirements it introduces for vault operators.

Learnings for Busy Readers

Short on time? Here are the key takeaways. For the full analysis and supporting data, continue reading below.

MiCA does not directly regulate DeFi protocols with no identifiable intermediary. What it comprehensively regulates are the operators, custodians, and service providers that interact with those protocols on behalf of EU clients. That indirect effect is the critical development for institutional DeFi allocation.

For vault operators, MiCA's CASP licensing requirements introduce mandatory governance standards around conflict of interest management, client asset safeguarding, and audit trail production. These requirements apply to any entity providing crypto-asset management services to EU clients, regardless of whether the underlying protocols are themselves regulated.

For institutional allocators, MiCA's conflict-of-interest framework scrutinises the commingling of curator and operator roles, which the first trilogy identified as a structural problem. MiCA Articles 68 through 73 require documented conflict of interest policies, auditable complaint processes, and controls for outsourcing risk. The curator-as-operator arrangement that characterises most DeFi vaults does not satisfy these requirements without additional governance infrastructure.

The Travel Rule adds a separate and immediate requirement. Since December 30, 2024, every crypto-asset transfer involving a CASP must be accompanied by full originator and beneficiary data. For DeFi vault transactions, producing that data requires infrastructure that most vault products were not designed to generate.

What MiCA Does and Does Not Cover

Understanding MiCA's scope precisely is the starting point for any serious analysis of its implications for DeFi vault allocation.

MiCA regulates crypto-asset service providers: exchanges, custodians, portfolio managers, transfer agents, and advisors operating in or serving clients in the EU. It requires CASP authorisation from a national competent authority, with EU-wide passporting once authorised. As of late 2025, over 50 CASPs had received MiCA authorisation across the European Economic Area, with Germany, the Netherlands, and Luxembourg attracting the largest concentrations of licensed entities.

MiCA does not regulate fully decentralised protocols. Where no identifiable entity manages the primary functions of a DeFi protocol, MiCA cannot be applied. The regulation acknowledges this explicitly. Protocols like Aave, Morpho, and Euler, where governance is distributed, and no single entity controls execution, are not in scope.

The boundary, however, is not always clean. MiCA applies a substance-over-form test: where a protocol has identifiable operators managing primary functions, the protocol may fall within scope regardless of how it characterises itself. More than 50% of DeFi protocols still lack clarity on their MiCA classification as of 2025. For vault operators with identifiable governance structures, the risk of falling within MiCA's scope is real and requires legal assessment rather than assumption.

What is unambiguous is that any entity providing crypto-asset portfolio management services to EU clients is a CASP under MiCA and must be authorised accordingly. A vault operator managing assets on behalf of institutional EU clients is providing a service that falls squarely within MiCA's CASP definition. The protocols the vault operator interacts with may not be regulated. The operator is.

What MiCA Requires of Vault Operators

For vault operators that fall within MiCA's CASP framework, the governance requirements are specific and operationally demanding.

Conflict of interest management

MiCA Articles 68 through 73 require CASPs to maintain documented policies identifying and managing conflicts of interest, auditable complaint processes, and controls for outsourcing risk. The curator-as-operator arrangement that characterises most DeFi vaults creates an immediate conflict of interest disclosure problem. A single entity designing the strategy, executing the rebalances, and managing the operator infrastructure has conflicts at every stage: the curator's TVL incentive, the performance fee structure, and the absence of independent oversight. MiCA does not prohibit these arrangements but requires that they be documented, disclosed, and managed through controls that can be demonstrated to a regulator. A vault operator who cannot produce that documentation has a compliance gap.

Client asset safeguarding

MiCA requires strict segregation and safeguarding of client funds, with daily reconciliation and documented controls for preventing misuse. For DeFi vault operators managing institutional assets, this requirement extends to the on-chain environment. The operator must be able to demonstrate, at any point, where client assets are held, in what protocols, at what valuations, and under what controls. A vault product that cannot produce this audit chain does not satisfy MiCA's safeguarding requirement.

Audit trail production

MiCA requires CASPs to maintain chronological, automatically recorded audit logs of all trades and instructions, in an easily searchable format. This is the compliance log requirement that the first trilogy identified as absent from most DeFi vault products. Under MiCA, it is not a best practice. It is a legal obligation for any CASP providing vault management services to EU clients.

DORA operational resilience

The Digital Operational Resilience Act applied from January 17, 2025, to all financial entities regulated under EU law, including MiCA-licensed CASPs. DORA requires documented ICT risk management frameworks, mandatory incident reporting, regular resilience testing, and oversight of third-party ICT providers. For vault operators whose infrastructure depends on third-party oracle providers, bridge infrastructure, or external data feeds, DORA introduces specific oversight obligations for each of those dependencies.

The institutional digital asset space moves fast. Our subscribers get structured analysis across staking, DeFi vaults, and regulation through DeFi Dispatch, Institutional Lens, DeFi Infrastructure for Institutions, andLegal Layer. No noise. Just the signals that matter. Subscribe to the newsletter at the bottom of this page.

What MiCA Requires of Institutional Allocators

For institutional allocators rather than operators, MiCA's implications operate at a different level. The allocator is typically not the CASP. But the allocator's counterparties are, and MiCA changes what those counterparties are required to provide.

Counterparty due diligence

An institutional allocator interacting with a DeFi vault through a MiCA-licensed custodian or service provider can rely on that intermediary's CASP authorisation as a baseline governance signal. But authorisation is a threshold, not a guarantee of mandate alignment. The allocator still needs to verify that the specific governance infrastructure of the vault product satisfies its own mandate requirements, including pre-execution controls, compliance log production, and role separation, beyond what MiCA's minimum requirements specify.

Travel Rule compliance

Since December 30, 2024, every crypto-asset transfer involving a CASP requires full originator and beneficiary data. For institutional allocators using a custodian to interact with DeFi vault protocols, the custodian bears the Travel Rule obligation. But the allocator needs to verify that the custodian's infrastructure can produce compliant transfer data for every vault interaction, including rebalances initiated by the curator. Many vault architectures do not generate the data structure that Travel Rule compliance requires, because the rebalance is initiated by a smart contract rather than a named originator. Identifying and resolving that gap is the allocator's due diligence responsibility.

Conflict of interest framework alignment

MiCA's conflict of interest requirements apply to the CASP that the allocator uses. But the allocator's own governance framework, particularly for regulated custodians and asset managers subject to MiFID II, AIFMD, or equivalent frameworks, extends those requirements to the underlying vault architecture. If the curator and operator of the vault are the same entity, the allocator's compliance function must be able to demonstrate that the resulting conflict of interest is identified, disclosed, and managed. That demonstration requires the vault to produce documentation that most current products do not generate.

MiCA as an Architecture Signal, Not Just a Compliance Checklist

The most important implication of MiCA for DeFi vault infrastructure is not the specific compliance requirements it introduces for CASPs. It is the signal those requirements send about where the market is heading.

MiCA represents the EU's decision to regulate crypto-asset services the same way it regulates traditional financial services. The governance requirements it introduces for vault operators, conflict of interest management, client asset safeguarding, audit trail production, and operational resilience are the same requirements that have applied to traditional delegated asset managers for decades under MiFID II. MiCA is not inventing new governance standards. It is extending existing ones into the on-chain environment.

Seven countries outside the EU are actively drafting MiCA-style regulations. The IOSCO principles that informed MiCA's design are being referenced in regulatory discussions in the United States, Singapore, and the United Kingdom. The institutional governance standard that MiCA formalises for the EU is becoming the reference standard for regulated institutional participation in on-chain capital markets globally.

For vault operators and institutional allocators, this means the governance infrastructure question is not a European compliance question. It is a question about where the global market for institutional on-chain capital is heading. The operators who build the governance layer now, with pre-execution controls, exportable compliance logs, and contractual role separation, will be positioned to serve institutional capital as the regulatory environment converges. The operators who treat MiCA compliance as a checkbox exercise will find the governance gap exposed in the next jurisdiction that formalises the same requirements.

Key Takeaway

MiCA does not regulate DeFi protocols. It regulates the operators and service providers that interact with those protocols on behalf of institutional clients, and it introduces governance requirements that map precisely onto the structural gaps the first trilogy of this series identified.

For vault operators, MiCA's conflict of interest, safeguarding, and audit trail requirements are not optional for any entity providing vault management services to EU clients. The curator-as-operator arrangement that characterises most DeFi vaults creates documentation and disclosure obligations that require governance infrastructure beyond what most current products provide.

For institutional allocators, MiCA changes the counterparty due diligence question. The allocator now needs to verify not just that their custodian or service provider is MiCA-authorised, but that the specific vault architecture they are accessing can satisfy MiCA's audit trail, Travel Rule, and conflict of interest requirements in practice.

The governance infrastructure that satisfies both requirements, pre-execution controls, exportable compliance logs, and contractual role separation, is the same infrastructure that the first trilogy established as the missing layer in DeFi vault architecture. MiCA makes building it a regulatory inevitability for operators serving EU institutional clients. The direction of travel for every other major jurisdiction suggests it will not remain a European requirement for long.

Next in this series: Travel Rule Enforcement and the Onchain Compliance Gap

Frequently Asked Questions (FAQs)

Does MiCA regulate DeFi protocols like Aave, Morpho, and Euler?

No, not directly. MiCA applies a substance-over-form test: fully decentralised protocols with no identifiable entity managing primary functions are excluded from its scope. Aave, Morpho, and Euler operate as decentralised protocols and are not directly regulated under MiCA. However, any entity providing crypto-asset portfolio management services using those protocols on behalf of EU clients is a CASP under MiCA and must be authorised accordingly. The protocols are not regulated. The operators using them to serve EU institutional clients are.

What is the MiCA CASP authorisation requirement, and who does it apply to?

Any entity providing crypto-asset services to EU clients, including portfolio management, custody, exchange, and transfer services, must obtain CASP authorisation from a national competent authority in an EU member state. Authorisation in one member state provides passporting rights across all 27 EU countries. Capital requirements range from €50,000 to €150,000, depending on the service type. As of late 2025, over 50 CASPs had received authorisation, with transitional arrangements for pre-existing providers expiring across member states by July 2026.

What does MiCA's conflict of interest requirement mean for DeFi vault operators?

MiCA Articles 68 through 73 require CASPs to maintain documented conflict of interest policies, auditable complaint processes, and outsourcing controls. For a vault operator where the curator and operator functions are held by the same entity, MiCA requires that the resulting conflicts be identified, documented, disclosed to clients, and managed through controls that can be demonstrated to a regulator. A vault operator that cannot produce this documentation has a compliance gap under MiCA, regardless of the quality of the underlying strategy.

What is the Travel Rule, and what does it require for DeFi vault transactions?

The Transfer of Funds Regulation, which implements the Travel Rule for crypto-asset transfers, became enforceable on December 30, 2024. It requires every crypto-asset transfer involving a CASP to be accompanied by full originator and beneficiary data: name, account identifier, address or national ID, and date of birth. For DeFi vault rebalances initiated by smart contracts rather than named originators, producing compliant Travel Rule data requires infrastructure that most vault architectures were not designed to generate. Institutional allocators need to verify that their custodian's infrastructure can produce this data for every vault interaction before initiating transactions.

How does MiCA interact with DORA for vault operators?

The Digital Operational Resilience Act applied from January 17, 2025, to all financial entities regulated under EU law, including MiCA-licensed CASPs. DORA requires documented ICT risk management frameworks, mandatory incident reporting to regulators, regular resilience testing, and oversight of third-party ICT providers. For vault operators whose infrastructure depends on external oracle providers, bridge infrastructure, or off-chain data feeds, DORA introduces specific oversight obligations for each dependency. Non-compliance with DORA carries the same enforcement consequences as non-compliance with MiCA, making it a parallel compliance obligation rather than a secondary one.

P2P.org builds the protection layer that sits between regulated institutions and DeFi execution environments, independently of the curators who manage allocation strategies. If you are evaluating the infrastructure requirements for a DeFi allocation program, talk to our team.

Disclaimer

This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or investment advice. Regulatory obligations may vary depending on jurisdiction and specific business activities. Readers should consult their own legal and compliance advisors regarding applicable requirements.

Subscribe to P2P-economy

Get the latest posts delivered right to your inbox

<h2 id="series-hub-institutional-staking"><strong>Series: Hub | Institutional Staking</strong></h2><p>The Institutional Staking Hub is <a href="http://p2p.org/?ref=p2p.org">P2P.org</a>'s definitive reference for institutions building proof-of-stake programs. From foundational concepts to infrastructure selection and risk architecture, each article addresses a specific operational or technical dimension that determines how a staking program performs in practice.</p><p>This is article 2 in the series. Read the foundation first: <a href="https://p2p.org/economy/what-is-institutional-staking/">What Is Institutional Staking? A Complete Guide for Funds, Custodians, and Treasury Teams</a></p><h2 id="learnings-for-busy-readers">Learnings for Busy Readers</h2><p>What this article covers:</p><ul><li>What validator infrastructure is and what it actually does at the network level</li><li>The difference between self-operated and delegated validator models</li><li>The technical components that determine whether infrastructure is institutional-grade</li><li>How key management architecture affects custody, risk, and compliance</li><li>What client diversity means and why it matters for operational resilience</li><li>How DVT changes the risk architecture of validator operations</li><li>The metrics and certifications that define institutional-grade validator providers</li><li>A due diligence checklist for evaluating validator infrastructure</li></ul><p>The core argument: Validator infrastructure is not a commodity. The operational decisions made at the infrastructure layer determine uptime, slashing exposure, reward outcomes, and compliance posture. Institutions that treat validator selection as a risk management decision consistently achieve better outcomes than those that treat it as a cost optimisation exercise.</p><h2 id="introduction">Introduction</h2><p>Most institutional conversations about staking start with reward rates. They should start with infrastructure.</p><p>Validator infrastructure is the operational layer that sits between an institution's capital and the proof-of-stake protocol it is participating in. It determines whether consensus participation is reliable or fragile, whether slashing exposure is managed or assumed, and whether the reporting an institution needs for accounting, audit, and compliance can actually be produced.</p><p>Major progress in validator infrastructure, institutional custody, multi-chain staking frameworks, and enterprise-grade reporting has made staking operationally viable at scale. For large asset managers, including pension funds, endowments, and conservative allocators, the legal uncertainty and operational risk that kept them on the sidelines are now falling away (Source: <a href="https://coinshares.com/us/insights/knowledge/institutional-staking-on-the-rise/?ref=p2p.org">CoinShares</a>).</p><p>But operational viability is not the same as operational quality. As institutions move from evaluation to deployment, the question changes from whether staking is viable to whether the infrastructure underpinning a specific staking program meets institutional standards. This article answers that question from the ground up.</p><h2 id="what-validator-infrastructure-is">What Validator Infrastructure Is</h2><p>In a proof-of-stake network, validators are the entities responsible for proposing and attesting to new blocks. They do not just hold staked capital. They run software, maintain network connections, sign messages, and participate in consensus rounds continuously. When a validator goes offline, misses attestations, or double-signs a message, the protocol responds with penalties. When a validator performs correctly, the protocol distributes rewards.</p><p>Validator infrastructure is everything that makes that participation happen reliably: the hardware or cloud architecture the validator software runs on, the key management system that controls signing credentials, the monitoring stack that detects and responds to anomalies, the client software that communicates with the network, and the reporting layer that captures everything for downstream use.</p><p>Ethereum supports over 1.1 million active validators in 2026, with average validator uptime near 99.2% across the network (Source: <a href="https://coinlaw.io/cryptocurrency-staking-statistics/?ref=p2p.org">CoinLaw</a>). That network average conceals significant variance between operators. In enterprise IT, Service Level Agreements (SLAs) define the expected uptime and reliability of a service provider. The blockchain space is increasingly moving in the same direction, especially as institutions explore staking as part of their portfolio strategy.</p><h2 id="self-operated-vs-delegated-validator-models">Self-Operated vs. Delegated Validator Models</h2><p>Institutions entering proof-of-stake networks have two structural choices for how they participate at the infrastructure layer.</p><h3 id="self-operated-validators"><strong>Self-operated validators</strong></h3><p>An institution builds and operates its own validator nodes. It controls the infrastructure, manages the keys, handles software updates, and monitors performance directly. This model gives maximum control and governance participation, but it carries the full operational burden. The institution must maintain the specialised engineering capability, 24/7 monitoring, incident response processes, and protocol expertise required to operate validators safely at scale.</p><p>Rather than hiring experts, provisioning hardware or cloud infrastructure, and securing forensic-grade security, institutions using a managed service can get their staking strategy up and running in weeks or less. The inverse is equally true: institutions that choose self-operation must be prepared to build all of that capability in-house.</p><h3 id="delegated-validator-infrastructure-staking-as-a-service"><strong>Delegated validator infrastructure (staking-as-a-service)</strong></h3><p>An institution delegates its capital to a professional validator operator. The institution retains custody of its assets at all times. The provider operates the infrastructure, manages keys, monitors performance, handles upgrades, and delivers reporting. This is the dominant model for institutional participation, as it removes the operational burden while preserving custody control.</p><p>The critical requirement in any delegated arrangement is non-custody. In a correctly structured staking-as-a-service model, the validator provider never holds the institution's assets. Assets are not transferred. Delegation happens at the protocol level, and the institution retains withdrawal authority.</p><h2 id="the-technical-components-of-institutional-grade-infrastructure">The Technical Components of Institutional-Grade Infrastructure</h2><p>Not all validator infrastructure is equivalent. The gap between consumer-grade and institutional-grade validator operations shows up across five technical dimensions.</p><figure class="kg-card kg-image-card kg-card-hascaption"><img src="https://p2p.org/economy/content/images/2026/05/_p2p-validator-infrastructure-stack-institutional.jpg" class="kg-image" alt="A four-layer vertical diagram showing the institutional validator infrastructure stack: Protocol Layer at the base, followed by Infrastructure Layer, Key Management Layer, and Reporting Layer at the top, each labelled with its primary function." loading="lazy" width="2000" height="1304" srcset="https://p2p.org/economy/content/images/size/w600/2026/05/_p2p-validator-infrastructure-stack-institutional.jpg 600w, https://p2p.org/economy/content/images/size/w1000/2026/05/_p2p-validator-infrastructure-stack-institutional.jpg 1000w, https://p2p.org/economy/content/images/size/w1600/2026/05/_p2p-validator-infrastructure-stack-institutional.jpg 1600w, https://p2p.org/economy/content/images/2026/05/_p2p-validator-infrastructure-stack-institutional.jpg 2240w" sizes="(min-width: 720px) 720px"><figcaption><i><em class="italic" style="white-space: pre-wrap;">The institutional validator infrastructure stack. Four layers from protocol to reporting, showing how each layer contributes to uptime, security, and compliance.</em></i></figcaption></figure><h3 id="hardware-and-network-architecture"><strong>Hardware and network architecture</strong></h3><p>Institutional validators operate on dedicated hardware rather than shared cloud infrastructure, with redundant power, connectivity, and compute. Professional validators target near-perfect uptime backed by strict SLAs. They utilise low-latency bare-metal hardware, high-throughput connectivity, and optimised client diversity to prevent network-wide bugs from causing local outages. Geographic distribution across multiple data centres reduces single-point-of-failure risk. Active/passive failover mechanisms ensure consensus participation continues through hardware or connectivity incidents.</p><h3 id="key-management-architecture"><strong>Key management architecture</strong></h3><p>Validator keys are the most sensitive operational asset in a staking program. There are two key types relevant to institutional operations: the signing key, used to participate in consensus, and the withdrawal key, used to access staked capital and rewards.</p><p>In an institutional non-custodial arrangement, the institution retains the withdrawal key at all times. The validator operator manages the signing key through a key management system designed to prevent the signing key from being exposed, duplicated, or used in ways that would trigger double-signing penalties. Hardware security modules, remote signing services, and key sharding approaches are all architectural choices at this layer.</p><h3 id="client-diversity"><strong>Client diversity</strong></h3><p>Every proof-of-stake network runs on consensus client software. On Ethereum, multiple independent client implementations exist, including Prysm, Lighthouse, Teku, Nimbus, and Lodestar on the consensus layer. The risk of running a single client in concentration is significant. The Prysm outage in December 2025, where validator participation dropped to approximately 75% and 248 blocks were missed, vividly demonstrated the risk posed by stakers herding toward a single consensus client.</p><p>Institutional-grade providers operate diversified client environments. If one client has a bug or outage, validators running alternative clients continue participating normally. This is a meaningful differentiator that does not appear in uptime statistics measured under normal conditions.</p><h3 id="monitoring-and-incident-response"><strong>Monitoring and incident response</strong></h3><p>Validator infrastructure requires continuous monitoring: block proposal success rates, attestation participation, peer connectivity, signing latency, and software version currency. Institutional-grade operations maintain 24/7 monitoring with defined escalation paths and incident response procedures. To avoid slashing, validators must operate secure, redundant, and highly available infrastructure. This includes implementing slashing protection mechanisms such as remote signing, key sharding, or sentry node architectures, and continuously monitoring node health, block production, and consensus participation metrics.</p><h3 id="reporting-and-audit-infrastructure"><strong>Reporting and audit infrastructure</strong></h3><p>Institutions need validator-level reward attribution for accounting, tax reporting, and audit purposes. This requires a reporting layer that captures rewards at the epoch level, attributes them to specific delegations, and delivers data in formats compatible with institutional back-office systems. Performance data, slashing history, and governance participation records all require structured capture. This layer is frequently underspecified in evaluations focused on uptime and fee rates.</p><h2 id="what-dvt-changes-about-validator-risk-architecture">What DVT Changes About Validator Risk Architecture</h2><p>Distributed Validator Technology (DVT) is a protocol-level mechanism that distributes the validator signing function across multiple independent nodes. Rather than a single node holding and using the signing key, DVT allows a threshold of nodes to collectively produce validator signatures. No single node has access to the complete key.</p><p>For institutional operations, DVT addresses two risk categories simultaneously. First, it eliminates single-point-of-failure at the signing layer. A hardware failure, network outage, or compromise of a single node does not disable the validator or expose the signing key. Second, it structurally prevents double-signing, since generating a duplicate signature requires a threshold of nodes to act simultaneously, which does not occur under normal failure conditions.</p><p>DVT is not yet universally deployed across all proof-of-stake networks, but its adoption is accelerating on Ethereum and represents a meaningful infrastructure maturity signal when evaluating providers.</p><h2 id="reward-mechanics-at-the-infrastructure-layer">Reward Mechanics at the Infrastructure Layer</h2><p>Protocol rewards are generated by the network, not by the validator provider. What the infrastructure layer controls is how efficiently those rewards are captured.</p><p>On Ethereum, rewards come from two sources: consensus layer rewards (base staking rewards for correct block proposals and attestations) and execution layer rewards (priority fees and MEV). Base ETH staking rewards generally range from 3% to 4%, while restaking incentives can temporarily lift combined yields above 8% to 15% (Source: <a href="https://coinlaw.io/cryptocurrency-staking-statistics/?ref=p2p.org">CoinLaw</a>).</p><p>Infrastructure quality affects reward capture in measurable ways. A validator with sustained 99.9% uptime captures consensus rewards on nearly every eligible slot. A validator with 98% uptime misses roughly 1 in 50 attestation opportunities. At scale, that difference compounds into material reward outcomes across a staking program.</p><p>MEV capture is a separate infrastructure consideration. Validators connected to MEV relays receive a share of transaction ordering value from block builders. Institutional operators must evaluate the MEV relay landscape for compliance implications, since certain relay types may route transactions in ways that conflict with regulatory obligations around transaction ordering.</p><p>Network conditions determine protocol-generated rewards and are variable. <a href="http://p2p.org/?ref=p2p.org">P2P.org</a> does not control or set reward rates.</p><h2 id="the-institutional-standard-certifications-audits-and-compliance-requirements">The Institutional Standard: Certifications, Audits, and Compliance Requirements</h2><p>For institutions operating under regulatory obligations, independent validation of validator infrastructure controls matters.</p><p>SOC 2 Type II is the most relevant independent security attestation for validator infrastructure providers. Enterprise clients typically want Type II reports because they demonstrate how controls perform in real operations, not just at a point in time. A SOC 2 Type II report covering availability and security criteria provides meaningful independent assurance that the controls governing validator uptime and key management are operating as documented. It is a floor, not a ceiling, but it is a meaningful one. <a href="http://p2p.org/?ref=p2p.org">P2P.org</a> achieved SOC 2 Type II certification in December 2025, independently validating our operational controls across security and availability criteria (Source: <a href="https://p2p.org/economy/validator-due-diligence-framework-what-institutions-really-need-to-evaluate/">P2P.org</a>).</p><p>ISO 27001 certification for information security management systems is a second relevant attestation, particularly for institutions operating under MiCA in Europe or with data governance obligations. Penetration testing records, incident disclosure history, and governance participation policies round out the compliance picture.</p><p>Institutional adoption of crypto risk frameworks has climbed to 78%, with custodial spend reaching $16 billion in 2025. Risk compliance ranks as the top priority for 84% of institutions. <a href="https://coinlaw.io/bitcoin-staking-statistics/?ref=p2p.org">CoinLaw</a> Validator infrastructure sits at the centre of that risk framework for any institution running a staking program.</p><h2 id="how-to-evaluate-validator-infrastructure-a-due-diligence-framework">How to Evaluate Validator Infrastructure: A Due Diligence Framework</h2><p>For a complete evaluation process, including the specific questions to ask and the mechanisms to assess, see our Validator Playbook article: <a href="https://p2p.org/economy/validator-due-diligence-framework-what-institutions-really-need-to-evaluate/">Validator Due Diligence: An Institutional Framework</a>.</p><p>The criteria below are the foundational dimensions any institutional evaluation must cover.</p><h3 id="infrastructure-architecture"><strong>Infrastructure architecture</strong></h3><ul><li>[ ] Does the provider operate dedicated hardware or shared cloud infrastructure?</li><li>[ ] Are data centres geographically distributed with documented failover?</li><li>[ ] What is the provider's SLA for validator uptime, and what is the documented track record?</li></ul><h3 id="key-management"><strong>Key management</strong></h3><ul><li>[ ] How are signing keys managed? Remote signing, HSM, or key sharding?</li><li>[ ] Does the institution retain withdrawal key control at all times?</li><li>[ ] What is the key recovery process in the event of a provider incident?</li></ul><h3 id="client-diversity-1"><strong>Client diversity</strong></h3><ul><li>[ ] Does the provider run multiple consensus clients across its validator fleet?</li><li>[ ] What is the distribution across client types, and how is this documented?</li><li>[ ] How does the provider respond to client-specific bugs or vulnerabilities?</li></ul><h3 id="slashing-risk-controls"><strong>Slashing risk controls</strong></h3><ul><li>[ ] What slashing protection mechanisms are in place?</li><li>[ ] What is the provider's slashing history across all networks they operate on?</li><li>[ ] Is there a documented incident response process specific to slashing conditions?</li></ul><h3 id="reporting-and-compliance"><strong>Reporting and compliance</strong></h3><ul><li>[ ] Can the provider deliver validator-level reward attribution at the epoch level?</li><li>[ ] Are reports available in formats compatible with institutional accounting systems?</li><li>[ ] Does the provider hold SOC 2 Type II or equivalent independent certification?</li></ul><h3 id="network-coverage-and-governance"><strong>Network coverage and governance</strong></h3><ul><li>[ ] Which proof-of-stake networks does the provider support?</li><li>[ ] How does the provider handle protocol governance participation on behalf of delegators?</li><li>[ ] What is the process for network upgrades and client version management?</li></ul><h2 id="where-p2porg-sits-in-this-architecture">Where <a href="http://p2p.org/?ref=p2p.org">P2P.org</a> Sits in This Architecture</h2><p><a href="http://p2p.org/?ref=p2p.org">P2P.org</a> operates non-custodial validator infrastructure across more than 40 proof-of-stake networks, supporting custodians, funds, ETF issuers, and treasury teams with institutional-grade staking programs. Our infrastructure operates on dedicated hardware with geographic distribution, client diversity across consensus implementations, and SOC 2 Type II certification achieved in December 2025.</p><p>Institutions retain full custody of their assets throughout. Validator-level reward reporting is available for accounting and audit requirements. Governance participation policies are configurable per delegation.</p><p>Explore our infrastructure and supported networks at <a href="https://p2p.org/?ref=p2p.org">p2p.org</a>.</p><p>Building an institutional staking program? <a href="http://p2p.org/?ref=p2p.org">P2P.org</a> provides non-custodial validator infrastructure across 40+ proof-of-stake networks, with validator-level reporting and operational safeguards designed for institutional requirements. <a href="https://p2p.org/?ref=p2p.org">Explore P2P.org Staking Infrastructure</a></p><h2 id="key-takeaway">Key Takeaway</h2><p>Validator infrastructure is the operational foundation of every institutional staking program. It determines uptime, slashing exposure, reward capture, reporting capability, and compliance posture. The decision of which infrastructure to operate or delegate to is a risk management decision, not a cost decision.</p><p>The institutions that will operate effective staking programs at scale are those that evaluate validator infrastructure with the same rigour they apply to any other mission-critical operational dependency. The checklist above is a starting point. The standard is set by the protocol and by the expectations of the risk committees, custodians, and regulators that govern institutional capital.</p><p>Network conditions determine protocol-generated rewards and are variable. <a href="http://p2p.org/?ref=p2p.org">P2P.org</a> does not control or set reward rates. Slashing risks are protocol-defined and client-borne. Operational safeguards are implemented to reduce slashing exposure but do not eliminate protocol-level risk.</p><h2 id="frequently-asked-questions">Frequently Asked Questions</h2><h3 id="what-is-validator-infrastructure-in-proof-of-stake-networks"><strong>What is validator infrastructure in proof-of-stake networks?</strong></h3><p>Validator infrastructure is the technical stack that enables participation in proof-of-stake consensus. It includes the hardware or cloud architecture the validator software runs on, the key management system that controls signing credentials, the monitoring and incident response stack, the consensus client software, and the reporting layer that captures performance and reward data. Validator infrastructure determines uptime, slashing exposure, reward capture, and compliance posture for any staking program.</p><h3 id="what-is-the-difference-between-self-operated-and-delegated-validator-infrastructure"><strong>What is the difference between self-operated and delegated validator infrastructure?</strong></h3><p>In a self-operated model, the institution builds and runs its own validator nodes, retaining full control but carrying the full operational burden, including specialised engineering, 24/7 monitoring, and protocol expertise. In a delegated model (staking-as-a-service), a professional validator provider operates the infrastructure while the institution retains custody of its assets at all times. The delegation happens at the protocol level, and the institution retains withdrawal authority. Most institutional participants use the delegated model.</p><h3 id="what-makes-validator-infrastructure-institutional-grade"><strong>What makes validator infrastructure institutional-grade?</strong></h3><p>Institutional-grade validator infrastructure operates on dedicated hardware with geographic redundancy, runs diversified consensus clients to avoid single-client failure risk, manages signing keys through hardware security modules or remote signing services, maintains 24/7 monitoring with documented incident response procedures, holds independent certifications such as SOC 2 Type II, and delivers validator-level reward reporting compatible with institutional accounting and audit requirements.</p><h3 id="what-is-distributed-validator-technology-and-why-does-it-matter-for-institutions"><strong>What is Distributed Validator Technology, and why does it matter for institutions?</strong></h3><p>DVT distributes the validator signing function across multiple independent nodes. No single node holds the complete signing key. A threshold of nodes must act together to produce a valid signature. This eliminates single-point-of-failure at the signing layer and structurally prevents double-signing, since triggering that condition requires a threshold of nodes to act simultaneously under failure conditions. For institutions, DVT is a meaningful risk reduction mechanism at the key management layer.</p><h3 id="how-do-validator-infrastructure-decisions-affect-reward-outcomes"><strong>How do validator infrastructure decisions affect reward outcomes?</strong></h3><p>Protocol rewards are determined by the network, not by the provider. However, infrastructure quality determines how efficiently rewards are captured. A validator with sustained 99.9% uptime captures consensus rewards on nearly every eligible slot. A validator with 98% uptime misses approximately 1 in 50 attestation opportunities. At the institutional scale, that gap compounds into material reward differences over time. MEV relay selection is a separate infrastructure consideration with both performance and compliance implications.</p><h3 id="what-certifications-should-institutions-look-for-in-a-validator-provider"><strong>What certifications should institutions look for in a validator provider?</strong></h3><p>SOC 2 Type II is the most relevant independent certification for validator infrastructure, as it validates how operational controls perform over time rather than at a single point in time. ISO 27001 is relevant for information security management, particularly under MiCA in Europe. Institutions should also request penetration testing records, incident disclosure history, and documentation of governance participation policies as part of their due diligence process.</p><h3 id="what-is-non-custodial-staking-and-why-is-it-required-for-institutional-programs"><strong>What is non-custodial staking, and why is it required for institutional programs?</strong></h3><p>In non-custodial staking, the institution's assets remain under the institution's control throughout the staking process. The validator provider operates infrastructure but never holds the assets. Withdrawal keys remain with the institution. In custodial staking, assets are transferred to the provider or a third-party custodian, which triggers additional regulatory obligations in most institutional compliance frameworks. Non-custodial architecture is the standard requirement for institutional staking programs because it preserves custody integrity and avoids the regulatory implications of asset transfer.</p><hr><p><strong><em>Disclaimer</em></strong></p><p>This article is provided for informational purposes only and does not constitute legal, regulatory, compliance, or investment advice. Regulatory obligations may vary depending on jurisdiction and specific business activities. Readers should consult their own legal and compliance advisors regarding applicable requirements.</p>

<p><strong>TL;DR:</strong><br>BitMart has launched staking products for ETH, SOL, and DOT, powered by P2P.org infrastructure. Users can now stake three of the largest proof-of-stake assets directly within their BitMart account. The integration runs on P2P.org's Unified Staking API — one connection covering multi-asset staking operations across all three networks simultaneously.</p><p>Staking has been one of the more fragmented corners of the exchange product stack. Offering it across multiple networks means dealing with different consensus mechanisms, different validator economics, different operational requirements per asset. ETH, SOL, and DOT are not interchangeable — each has its own architecture and its own edge cases.</p><p>BitMart launched all three at once. </p><p>That outcome is a direct function of how the integration was built.</p><h2 id="the-infrastructure-side-p2porgs-unified-staking-api"><strong>The Infrastructure Side: P2P.org's Unified Staking API</strong></h2><p>The technical foundation of this integration is P2P.org's Unified Staking API.</p><p>One connection covers ETH, SOL, and DOT — stake, unstake, sign, and retrieve data through a single endpoint. That's why BitMart was able to launch all three networks at once rather than phasing them in one at a time.</p><p>The API is built for exactly this use case. Exchanges and custodians connecting to it get access to P2P.org's validator infrastructure across multiple proof-of-stake networks without maintaining separate staking connections per asset. New networks follow the same standard, so expanding coverage doesn't require starting from scratch each time.</p><p>On the operational side, P2P.org runs the validators. The infrastructure is the same that serves regulated custodians and asset managers on the institutional side — $10B+ in staked assets, 190+ institutional clients, active across 40+ networks.</p><h2 id="why-eth-sol-and-dot"><strong>Why ETH, SOL, and DOT</strong></h2><figure class="kg-card kg-image-card"><img src="https://p2p.org/economy/content/images/2026/04/1600x900--1--2.png" class="kg-image" alt="" loading="lazy" width="1600" height="900" srcset="https://p2p.org/economy/content/images/size/w600/2026/04/1600x900--1--2.png 600w, https://p2p.org/economy/content/images/size/w1000/2026/04/1600x900--1--2.png 1000w, https://p2p.org/economy/content/images/2026/04/1600x900--1--2.png 1600w" sizes="(min-width: 720px) 720px"></figure><p>The asset selection reflects where staking demand is deepest. Ethereum is the largest proof-of-stake network by value staked globally. Solana has one of the most active retail staking ecosystems, with short reward cycles and straightforward delegation mechanics. provides protocol-level rewards to participants — P2P.org's position as an established DOT nominator matters here in a way it doesn't on simpler networks.</p><p>Together, these three assets cover the range of what exchange users are most likely to want to stake. BitMart's global user base — concentrated across Asia, Europe, and emerging markets — maps well to demand for all three.</p><h2 id="what-this-enables"><strong>What This Enables</strong></h2><p>BitMart's launch is a concrete example of what multi-network staking looks like when the infrastructure layer is already built. One API integration, three networks live simultaneously, validator operations handled by a provider with institutional-grade infrastructure behind it.</p><p>For BitMart users, the result is straightforward: staking rewards on three major PoS networks, accessible directly within the platform they already use to trade.</p><p><strong>Exchanges and custodians interested in adding staking to their product can learn more about P2P.org's Unified Staking API at</strong><a href="https://p2p.org/products/api?ref=p2p.org"><strong> </strong></a><a href="http://p2p.org/products/api?ref=p2p.org"><strong><u>p2p.org/products/api</u></strong></a><strong>.</strong></p><p>Disclaimer: Staking services may not be available in all jurisdictions. Staking rewards are variable and depend on network conditions. Digital assets involve risk, including possible loss of principal. BitMart does not provide investment, legal, or tax advice. </p><p><strong>FAQ </strong></p><p>Q: What is BitMart staking powered by? A: BitMart's ETH, SOL, and DOT staking products are powered by P2P.org, a non-custodial staking infrastructure provider with $10B+ in assets staked across 40+ networks.</p><p>Q: Which assets can I stake on BitMart with P2P.org? A: BitMart currently supports staking for ETH (Ethereum), SOL (Solana), and DOT (Polkadot) via the P2P.org integration.</p><p>Q: How does P2P.org's Unified Staking API work? A: The Unified Staking API gives exchanges and custodians access to P2P.org's staking infrastructure across multiple proof-of-stake networks through a single integration. Stake, unstake, sign, and retrieve data through one endpoint — covering multiple networks without a separate build per asset.</p>

ALL

Agoric

Aptos

Auth

Avail

Avalanche

Axelar

Babylon

Bitcoin

BTC

capital flow

Cardano

Celestia

certifications

Chainlink

compliance

Cosmos

Crescent

curator

Cyberway

DAOBet

Data stream

DeFi

defi dispatch

defi infrastrcuture

defi infrastructure

defi news

defi vault

due diligence

DVT

Dymension

Economy

Education

EigenLayer

Elrond

employee

employee advocacy

employee interviews

Ethereum

Evmos

exit queue

Explain Like I'm Five

Governance

Guide

hedge fund

how to

HR

HUB series

Hyperliquid

infrastructure

institutional lens

Kava

Kusama

landing

legal layer

Lido

liquid staking

LSP

Manta

Mantle

Marlin

Matic

MiCA

Moonbeam

MultiversX

Near

Networks

News

NuCypher

Oasis

Obol

Origin

P2P Verified

Partnership

pectra

Persistence

playbook

Pocket

Polkadot

Polygon

product

products

Quicksilver

Regen

regulation

Renzo

restaking

RPC Node

Sender

Serum

slashing

Solana

SSV

SSV.Network

ALL

Agoric

Aptos

Auth

Avail

Avalanche

Axelar

Babylon

Bitcoin

BTC

capital flow

Cardano

Celestia

certifications

Chainlink

compliance

Cosmos

Crescent

curator

Cyberway

DAOBet

Data stream

DeFi

defi dispatch

defi infrastrcuture

defi infrastructure

defi news

defi vault

due diligence

DVT

Dymension

Economy

Education

EigenLayer

Elrond

employee

employee advocacy

employee interviews

Ethereum

Evmos

exit queue

Explain Like I'm Five

Governance

Guide

hedge fund

how to

HR

HUB series

Hyperliquid

infrastructure

institutional lens

Kava

Kusama

landing

legal layer

Lido

liquid staking

LSP

Manta

Mantle

Marlin

Matic

MiCA

Moonbeam

MultiversX

Near

Networks

News

NuCypher

Oasis

Obol

Origin

P2P Verified

Partnership

pectra

Persistence

playbook

Pocket

Polkadot

Polygon

product

products

Quicksilver

Regen

regulation

Renzo

restaking

RPC Node

Sender

Serum

slashing

Solana

SSV

SSV.Network